Here’s something most people don’t want to admit. A lot of Texans have thought about getting life insurance, told themselves they’d handle it “soon,” and then let months or even years go by without doing anything about it.

It’s not laziness. Life gets busy. And honestly, the subject itself feels heavy. Nobody loves sitting down to think about what happens after they’re gone.

But here’s the thing. The families who struggle most after a loss are almost always the ones who had that same conversation and kept putting it off. The ones who are okay, financially at least, usually had a plan in place. It really is that straightforward.

If you live in Texas and you’ve been meaning to sort out your life insurance situation, this guide is for you. We’ll walk through everything you need to know, from how the different policies work to what questions you should be asking before you sign anything.

What Life Insurance Actually Does (And Why Texas Families Need It)

Life insurance is a contract. You pay into it regularly, and if you pass away while the policy is active, the insurance company pays a benefit to whoever you’ve named, your spouse, your kids, a business partner, whoever you choose.

That payout can be used for anything. Most people think of it as covering funeral expenses, and yes, it covers that. But the real value is everything else. The mortgage that still has 22 years left on it. The income your family depended on. The college fund you hadn’t finished building. The business loan with your name on it.

Texas has specific reasons why this matters more than people often realize. The state is growing fast, with families planting roots in the DFW area, Houston suburbs, and smaller cities across the state. A lot of those families are carrying significant financial obligations, mortgages, car payments, and in many cases, running their own businesses on top of everything else.

Add to that the fact that Texas has a large population of self-employed workers and independent contractors who don’t have employer-provided life insurance. Nobody is handing you a group plan when you’re your own boss. That coverage has to come from somewhere, and for most people, that means getting a private policy.

Working with licensed insurance agents in Texas means you get advice that actually reflects how the state’s laws and insurance market work. Not generic guidance written for a national audience that may not apply to your situation at all.

The Different Types of Life Insurance Policies in Texas

Not every policy is built the same, and choosing the wrong type is one of the more common mistakes people make. Here’s what’s actually available and who each one tends to serve well.

Term Life Insurance in Texas

Term life is the most straightforward policy you can get. You pick a coverage amount and a period of time, usually 10, 20, or 30 years. You pay your premium each month, and if you die during that window, your beneficiaries receive the death benefit. If you outlive the policy, it ends with no payout.

No mystery to it. No investment component. Just coverage for a defined period.

That simplicity is actually a feature, not a flaw. Term life insurance in 2025 continues to be widely used by young families, first-time homebuyers, and business owners who need solid coverage during the years when their financial obligations are at their highest. It also gives you the largest death benefit relative to what you put in.

Term life insurance tends to work best for:

- Parents with young children who need income replaced for the next 20 or more years

- Homeowners who want coverage that lines up with their mortgage payoff timeline

- Business owners protecting a key employee or securing a business loan

- Anyone who wants clear, straightforward coverage for a specific period of time

One thing worth knowing: the earlier you lock in a term policy, the better. Life insurance underwriting is heavily based on your age and health at the time you apply. Getting covered while you’re younger and in good health gives you access to stronger options down the road.

Whole Life Insurance

Whole life is a permanent policy. It doesn’t expire as long as you keep paying your premiums, and it builds cash value over time at a fixed rate. That cash value is real money you can borrow against while you’re still alive.

It serves a different purpose than term insurance. Whole life is often the right fit for people who want coverage that follows them through retirement, or who are using life insurance as part of a broader estate plan. Understanding how the right life insurance can reduce estate taxes becomes particularly important for high-net-worth families looking to preserve wealth across generations. Business owners also use it for buy-sell agreements, where the policy funds a buyout if one partner passes away unexpectedly.

Whole life tends to make sense for:

- People who want permanent coverage that doesn’t have an expiration date

- Those building a legacy or working through estate planning

- Business owners funding buy-sell partnership agreements

- Individuals who have maxed out other long-term savings options

Universal Life Insurance

Universal life is also permanent, but it gives you more flexibility than a traditional whole life policy. You can adjust your premium payments and your death benefit over time as your situation changes. The cash value grows, though the rate can vary depending on the policy type and market conditions.

For someone whose income fluctuates, a commission-based professional, a contractor, a small business owner with variable revenue, universal life offers a way to maintain permanent coverage without being locked into a rigid payment structure.

Final Expense Insurance

Final expense is a smaller whole life policy built for one specific purpose: covering the costs that come at the end of life. Funeral arrangements, outstanding medical bills, similar expenses. Coverage amounts are more modest than standard policies, and the application process is typically simpler with no medical exam required.

This type of policy is popular among older Texans who want to make sure their family isn’t left scrambling to cover those immediate costs during an already difficult time. It’s not designed to replace income or pay off a mortgage. It’s about relieving your family of one less burden when they’re grieving.

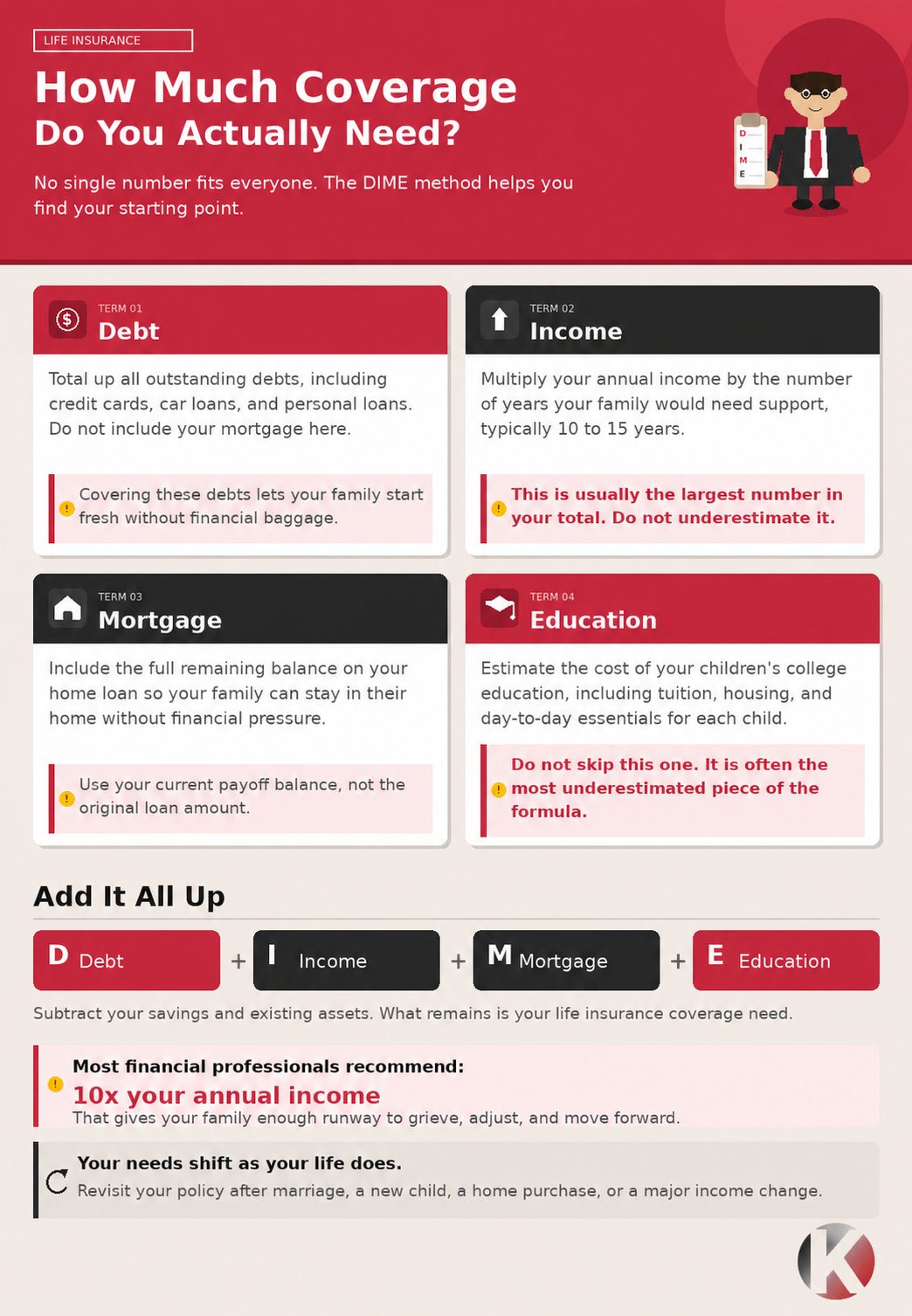

How Much Coverage Do You Actually Need?

This question comes up constantly, and there’s no single number that fits everyone. But there’s a framework that helps most people get into the right ballpark. It’s called the DIME method.

Debt: Total up your outstanding debts, not including your mortgage

Income: Multiply your annual income by the number of years your family would need support, typically 10 to 15

Mortgage: Include the full remaining balance on your home loan

Education: Estimate what it would take to cover your children’s college education

Add those numbers together, subtract any savings or assets your family could draw on, and you have a solid starting point.

Most financial professionals land on something close to 10 times your annual income as a general benchmark. The idea is to give your family enough runway to adjust, to grieve, to figure out next steps, without having to make desperate decisions at the worst possible time.

Your needs will also shift as your life does. A couple with no kids and a small mortgage has different coverage needs than that same couple a decade later with two children, a larger home, and a growing business. Doing a yearly insurance policy review helps ensure your coverage evolves with your life circumstances.

What Texas Law Says About Life Insurance

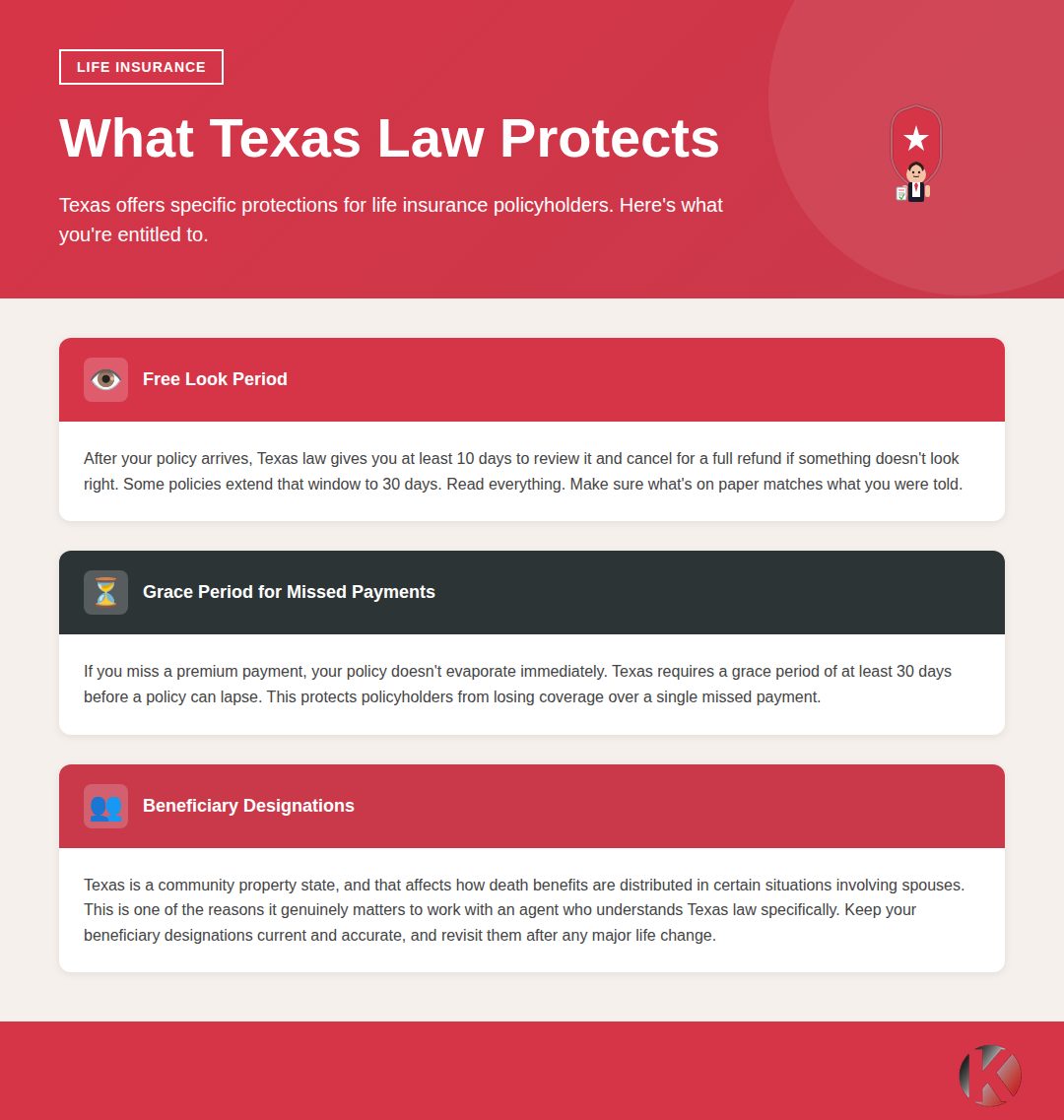

Texas has a well-organized regulatory structure for insurance, and it includes some strong consumer protections that every policyholder should know about.

The Texas Department of Insurance, known as the TDI, oversees every licensed insurance company and agent in the state. Any carrier or agent offering life insurance in Texas must be licensed through the TDI. When you’re comparing insurance companies in Dallas, Texas or anywhere else in the state, verifying their license is the first thing to check before you commit to anything.

Free Look Period: After your policy arrives, Texas law gives you at least 10 days to review it and cancel for a full refund if something doesn’t look right. Some policies extend that window to 30 days. Read everything. Make sure what’s on paper matches what you were told.

Grace Period for Missed Payments: If you miss a premium payment, your policy doesn’t evaporate immediately. Texas requires a grace period of at least 30 days before a policy can lapse. This protects policyholders from losing coverage over a single missed payment.

Beneficiary Designations: Texas is a community property state, and that affects how death benefits are distributed in certain situations involving spouses. This is one of the reasons it genuinely matters to work with an agent who understands Texas law specifically. Keep your beneficiary designations current and accurate, and revisit them after any major life change.

Life Insurance for Different Situations Across Texas

Life insurance doesn’t look the same for everyone. Here’s how it tends to play out for some of the more common situations we see across the state.

Families in the DFW Area

The Dallas-Fort Worth Metroplex is one of the most active housing markets in the country. Families are buying homes in Frisco, Keller, Grapevine, Allen, and dozens of communities around the metro. With that comes real financial exposure: a mortgage, often two working adults, and children who depend entirely on the household income.

If something happened to one of those earners, the financial impact would be immediate and severe. Life insurance gives the surviving family members the ability to stay in their home, keep their plans intact, and not face a financial crisis layered on top of everything else.

For most DFW families, choosing the right insurance coverage for your growing family starts with term life insurance in Texas. It covers the years of highest financial obligation and provides meaningful protection during the time it matters most. Exploring your insurance needs as a Dallas-Fort Worth resident helps you understand what specific protections make sense for your household.

Small Business Owners

Texas has one of the highest concentrations of small business owners in the country. If you run a business, your personal finances and your business finances are often more connected than you realize.

There are a few life insurance applications every Texas business owner should understand:

- Key Person Coverage: If a key employee or owner died suddenly, what would that do to your business? Key person insurance provides resources to help the business absorb that loss, cover transition costs, and keep operating.

- Buy-Sell Agreements: If you have a business partner, a properly funded buy-sell agreement means the surviving partner has what they need to buy out the deceased’s share cleanly. Without it, that situation becomes complicated and painful very quickly.

- Business Loan Collateral: Some Texas lenders require life insurance as part of a loan agreement. Term life is commonly used for this purpose.

- Premium Financing: Some business owners use premium financing strategies to carry larger life insurance policies without tying up significant working capital. If you’re considering this approach, understanding common misconceptions about premium financing helps you make an informed decision. It’s a specialized approach best explored with an experienced brokerage.

Truckers and Owner-Operators

The transportation industry is a backbone of the Texas economy, and independent truckers and owner-operators face above-average risk every single day. Unlike employees at larger companies, they typically have no employer-provided benefits at all.

That means life insurance is entirely on them to arrange. At Keen Coverage, we have an entire division focused on the trucking and transportation industry. We understand how owner-operators work, and we can help you find coverage that fits your situation without making the process more complicated than it needs to be.

Seniors in Texas

There’s a common assumption that once you reach a certain age, life insurance either isn’t available or isn’t worth pursuing. That assumption is often wrong.

Final expense policies are widely available to seniors with simplified underwriting and no medical exam required. If you purchased a whole life policy earlier in life, it continues providing coverage well into your later years. And term policies are still accessible for many people in their 60s who are in reasonable health.

For those approaching or already in retirement, life insurance also plays a meaningful role in estate planning. A properly structured policy can pass a tax-free benefit to your heirs and help cover estate-related expenses that might otherwise chip away at what you leave behind. Many seniors work with advisors who understand the differences between revocable vs. irrevocable life insurance trusts to maximize the benefit their beneficiaries receive while minimizing estate tax exposure.

Life Insurance and the Bigger Financial Picture

Life insurance rarely works in isolation. For most Texans, it’s one part of a broader financial strategy.

Life Insurance and Annuities

These two products are often paired because they solve opposite problems. Life insurance protects your family if you die too soon. Annuities protect you financially if you live longer than expected, by providing a reliable income stream through retirement.

Before committing to an annuity, it’s worth understanding whether annuities are worth it for your specific situation. Contrary to popular belief, annuities aren’t only for seniors—many younger adults use them as part of a comprehensive retirement strategy. Some investors even explore the laddering strategy with staggered annuities to optimize returns over time.

If you’re considering annuities, be aware of 5 common mistakes to avoid when shopping that could cost you thousands in the long run.

We offer both at Keen Coverage, and we can help you think through how they fit together so you’re not just covered in one direction.

Life Insurance and Long-Term Care

This one catches people off guard more than almost anything else. Nursing home care, in-home care, and assisted living are real financial risks that can drain retirement savings in a hurry if there’s no plan in place.

Timing matters significantly—knowing when is the right time to buy long-term care insurance can save you money and ensure you qualify before health issues arise. Understanding how long-term care insurance protects retirement savings helps you see it as part of your overall financial security plan, not just another expense.

Some life insurance policies now include long-term care riders, which let you access a portion of your death benefit early if you need that kind of care. It’s a flexible approach that addresses two different risks with one policy, and it’s worth asking about when you’re reviewing your options.

Life Insurance and Disability Insurance

Here’s something that surprises most people: statistically, you’re more likely to experience a serious disability before age 65 than you are to die before that age. Yet most people carry life insurance, and nothing to protect their income if they can’t work.

Life insurance takes care of your family if you’re gone. Disability insurance takes care of your income if you’re injured or ill and can’t earn a living. Both situations can devastate a household financially. Understanding how disability insurance complements workers’ compensation is essential, especially for self-employed Texans who don’t have employer-provided coverage.

Unfortunately,disability insurance myths often prevent people from getting the protection they need. One critical detail many people overlook is the own-occupation clause, which determines whether you’re covered if you can’t perform your specific job versus any job. Most insurance professionals recommend having both life and disability coverage in place.

How to Actually Choose the Right Policy

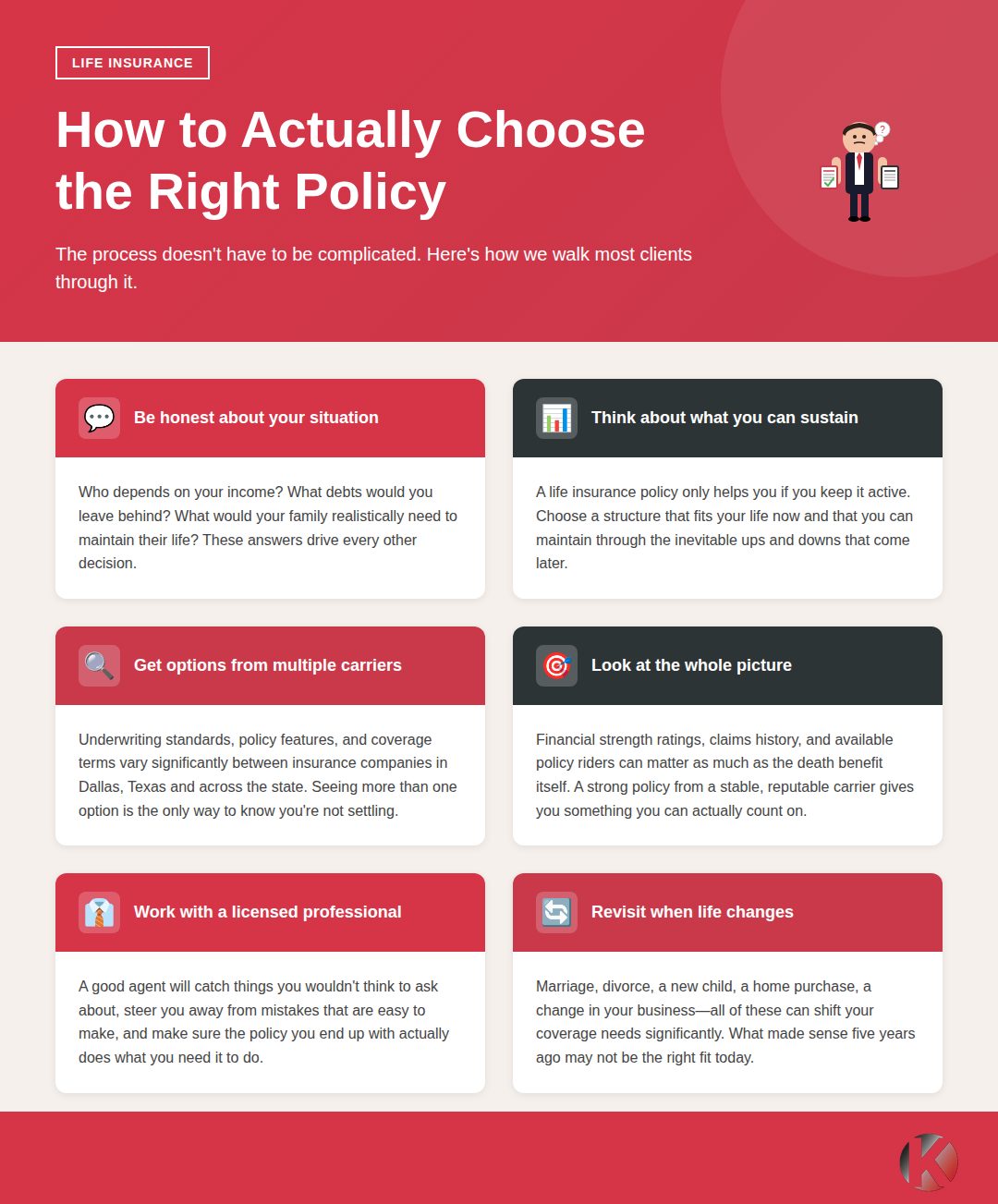

The process doesn’t have to be complicated. Here’s how we walk most clients through it.

Start by being honest about your situation: Who depends on your income? What debts would you leave behind? What would your family realistically need to maintain their life? These answers drive every other decision.

Think about what you can realistically sustain: A life insurance policy only helps you if you keep it active. Choose a structure that fits your life now and that you can maintain through the inevitable ups and downs that come later.

Get options from more than one carrier: Underwriting standards, policy features, and coverage terms vary significantly between insurance companies in Dallas, Texas and across the state. Seeing more than one option is the only way to know you’re not settling for less than what’s available to you.

Look at the whole picture, not just the coverage amount: Financial strength ratings, claims history, and available policy riders can matter as much as the death benefit itself. A strong policy from a stable, reputable carrier gives you something you can actually count on.

Work with a licensed professional who specializes in this: A good agent will catch things you wouldn’t think to ask about, steer you away from mistakes that are easy to make, and make sure the policy you end up with actually does what you need it to do.

Revisit your coverage when life changes: Marriage, divorce, a new child, a home purchase, a change in your business, all of these can shift your coverage needs significantly. What made sense five years ago may not be the right fit today.

Why Work with an Independent Brokerage?

There’s a meaningful difference between a captive agent who represents one insurance company and an independent brokerage that works for you.

At Keen Coverage, we are not locked into any single carrier’s product lineup. When you come to us, we’re looking across multiple insurance companies in Dallas, Texas and beyond to find the policy that actually fits your situation. Our recommendations aren’t shaped by a quota or a preferred product. They’re shaped by what makes sense for you specifically.

We’re an independent insurance brokerage serving clients across the Dallas-Fort Worth Metroplex, with offices in Fort Worth, Hurst, and Grapevine. Our team of licensed insurance agents in Texas holds credentials in both property and casualty and life and health insurance, so whether you need personal life coverage, business protection, or a combination of both, you’re getting guidance from people who’ve worked through all of it.

We’ve helped young families buying their first homes, business owners protecting what they’ve spent years building, truckers who need coverage that doesn’t add complexity to an already demanding schedule, and seniors working through what life insurance means for their estate plan. Every situation is different, and we treat it that way.

Mistakes That Are Worth Avoiding

Most of the mistakes people make with life insurance are avoidable once you know what to look out for.

Waiting too long: This is the most common one. Life insurance becomes harder to qualify for as you age, and health changes can close doors that were wide open before. The right time to get covered is before you need to work hard to qualify.

Underestimating what your family would actually need: It’s easy to pick a coverage number that sounds reasonable without really running the math. Use the DIME framework. Be honest about your household’s actual expenses and obligations.

Forgetting to update your beneficiaries: People go through divorces, remarriages, and losses. If your beneficiary designations are out of date, the payout may not go where you intend. Review them after any significant life event.

Not reading what you’re signing: Life insurance policies have real details in them. Exclusions, riders, conversion provisions, lapse terms. A careful read before you sign protects you from unpleasant surprises later.

Skipping riders that might matter: Add-ons like a waiver of premium, accelerated death benefits, or a conversion option can make a real difference in how the policy performs if your circumstances shift. It’s worth asking about them upfront.

Frequently Asked Questions About Life Insurance in Texas

Texas residents can access term life, whole life, universal life, and final expense insurance, among others. The right fit depends on your goals, how long you need coverage, and your overall financial picture. Talking with a licensed independent broker is the most efficient way to figure out which direction makes sense for your specific situation.

It depends on the policy type. Traditionally underwritten policies usually involve a medical exam. Simplified issue and guaranteed issue policies skip that step. Final expense insurance, which is popular among seniors, is typically available without any exam and has a relatively simple application process.

Often yes. Conditions like well-managed diabetes, controlled high blood pressure, or a past history of certain illnesses don’t automatically disqualify you. Different carriers use different underwriting standards, and knowing which ones are more favorable for specific health profiles is part of what we do at Keen Coverage. We work to match you with the carrier that’s the best fit for your situation.

Your policy stays in force. Life insurance is a contract, and relocating doesn’t void it. You should update your address with your insurance company and use the move as an opportunity to review whether your coverage still matches your current needs.

In most cases, life insurance death benefits are received income-tax free by beneficiaries. Texas also has no state income tax, which is an added benefit. Larger estates may have federal estate tax considerations, which is one reason estate planning matters and why it’s worth discussing your situation with both an insurance professional and a financial advisor.

A captive agent works for one specific insurance company and can only offer that company’s products. As an independent broker, we at Keen Coverage represent you. We work with multiple carriers and find the option that genuinely fits your needs, rather than fitting your needs into whatever one company happens to offer.

The Right Coverage Changes Everything

Nobody buys life insurance because it’s enjoyable. You buy it because you’ve thought about the people in your life and decided their security is worth doing something about.

The right policy doesn’t just provide a payout. It keeps a mortgage paid. It puts kids through school. It lets a spouse stay in their home. It keeps a business running. None of that is a small thing.

If you’re ready to stop putting this off, we’re here to make the process as clear and honest as it should be. Our licensed insurance agents in Texas will take the time to understand your situation, walk you through your real options, and help you find coverage that genuinely fits. No pressure, no unnecessary jargon, just straightforward guidance from people who handle this every day.

Ready to get started?

Reach out to us today for a consultation. Whether you’re comparing plans for the first time or revisiting coverage you already have, we’re here to help you land on a decision you feel good about.

This article is for informational purposes only and does not constitute legal or financial advice. Coverage options and eligibility vary by carrier and individual circumstances. Please consult a licensed insurance professional like Keen Coverage for guidance specific to your situation.

Related Posts

Term Life vs. Whole Life Insurance: Which Is Right for You?

What Is a Life Insurance Beneficiary and How Do You Choose One?

Life Insurance for Self-Employed Professionals in Texas

Long-Term Care Insurance vs. Life Insurance: What’s the Difference?

Life Insurance in Dallas: What Texas Residents Should Know

10 Mistakes to Avoid When Buying Life Insurance in Texas

How to Switch Life Insurance Policies Without Losing Coverage