Switching life insurance policies sounds simple enough, right? Cancel the old one, sign up for a new one, done.

Except that’s exactly how people end up with coverage gaps. Or lose thousands in accumulated value. Or discover they can’t actually qualify for the new policy they thought they could get.

We’ve watched this happen to Texas families more times than we can count. Someone gets frustrated with their current policy and jumps ship without thinking it through. Three months later they’re scrambling to fix a mess that could’ve been avoided with better planning.

Here’s a real example. A guy in Houston decides his whole life policy is too expensive. It makes sense, he wants to save some money. So he cancels it and applies for term coverage. Sounds logical. The problem is, he developed high blood pressure since his original policy. The new company either denies him or quotes him way higher than expected. Now he’s got no coverage at all because he already cancelled the first policy.

Or take the Dallas couple who switched policies to get better features. They did everything right, and got approved for the new coverage. But they cancelled their old policy the same day they applied for the new one. The new policy had a two-year contestability period. Six months later, the husband passes away unexpectedly. The insurance company finds a minor health disclosure issue and denies the claim. The family gets nothing.

These aren’t scary stories. This is what actually happens when people don’t know the right way to switch.

The good news? Switching life insurance policies can absolutely make sense. You just need to do it correctly. And that’s what we’re going to walk through right here.

Why People Switch Life Insurance Policies in Texas

Let’s start with the obvious question. Why switch at all?

Lots of reasons, actually. Your old policy might not fit your life anymore. Maybe you bought it 15 years ago when you were single. Now you’ve got kids and a mortgage and that coverage amount looks pretty weak.

Or maybe you’ve gotten healthier since you bought your original policy. Lost weight, quit smoking, got your diabetes under control. Your current policy reflects your old health status. A new policy could give you better rates based on who you are now.

Sometimes it’s about policy type. You bought a whole life when you were 25 because that’s what the agent recommended. Twenty years later you realize, term would’ve been smarter and cheaper. Or the flip side happens too. You’ve got term coverage that’s about to expire and now you want permanent coverage for estate planning.

Then there’s the straightforward stuff. You found better coverage with another company. Your current insurer’s customer service is terrible. Your financial situation changed and you need different features or riders.

All valid reasons to consider switching.

But here’s what matters most. Switching makes sense when the new policy genuinely improves your situation. It doesn’t make sense just because some agent cold-called you with what sounds like a better deal.

When You Should NOT Switch Your Life Insurance Policy

Before we get into how to switch, let’s talk about when you shouldn’t.

Your health got worsen since you bought your original policy. This is huge. If you’ve developed health conditions, gained significant weight, started medications, or gotten older with new issues, switching might hurt you. Your original policy locked in rates based on your health at that time. A new policy will price you based on your current health. That could mean higher rates or even denial.

Your original policy has significant cash value. This applies to permanent policies like whole life or universal life. If you’ve built up cash value over the years, switching means potentially losing that accumulated value or facing surrender charges. Sometimes it makes sense anyway, but you need to run the actual numbers.

You’re in the contestability period of your current policy. Every life insurance policy has a two-year contestability period when the insurance company can investigate claims more closely. If you’re still in that window, think twice about switching. You’d be starting another two-year period with a new policy.

The new policy isn’t actually better. Agents sometimes push people to switch when it doesn’t really benefit the customer. They just want the commission. If the new policy offers essentially the same coverage with the same features and similar rates, why bother with the hassle and risk?

You’re dealing with a serious health issue right now. If you’ve got an active cancer diagnosis, recent heart problems, or other major medical situations, now’s not the time to switch. Wait until you’re stable and cleared before applying for new coverage.

The Right Way to Switch Life Insurance Policies

Alright, here’s the process that actually works. Follow these steps in this exact order.

Step 1: Figure Out What You Actually Need

Before you do anything else, get clear on why you’re switching and what you need from a new policy.

What coverage amount do you actually need now? Has your mortgage gone up or down? Kids closer to college or already graduated? Income changed significantly? Run the numbers fresh. Don’t just assume you need the same amount as your old policy.

What type of policy makes sense? If you had a whole life, but really just need coverage for another 20 years, term might work better. If you have a term that’s expiring and you want guaranteed lifetime coverage, permanent might be the move.

What features and riders matter to you? Accelerated death benefit? Waiver of premium? Conversion options? Make a list of what you actually want.

Step 2: Check Your Current Health Status

Your health is the biggest factor in whether switching makes sense.

Think about what’s changed since you bought your original policy. Are you healthier or less healthy? Lost weight or gained it? Quit smoking or started? New medications or conditions?

If you’re not sure, talk to your doctor. Get current numbers on your blood pressure, cholesterol, weight, all that stuff. This gives you a realistic picture of how you’ll be rated.

Insurance agents in Texas can sometimes give you a preliminary assessment based on your health info. They know how different insurance companies in Dallas Texas rate different conditions. This helps you know what to expect before you actually apply.

Step 3: Shop for New Coverage (But Don’t Cancel Anything Yet)

Now you can start looking at new policies. Key word: looking. You’re not cancelling anything at this stage.

Get quotes from multiple carriers. Work with insurance agencies in Texas that represent several companies, not just one. This is important because different companies rate health conditions differently. One carrier might love you, another might not.

Compare the actual features, not just the monthly premium. What’s the death benefit? What riders are included? How’s the company’s financial rating? What’s their reputation for paying claims?

Read the fine print on the new policy. Understand the contestability period, the suicide clause, any exclusions or limitations. Make sure you know exactly what you’re getting into.

Step 4: Apply for the New Policy

Once you’ve found a policy that legitimately works better for you, apply for it. But here’s the critical part. You’re applying for new coverage. You’re not cancelling your old coverage. Not yet.

Complete the application honestly and thoroughly. Remember everything we said about being truthful on applications. This matters even more when you’re switching because you’ve got existing coverage to fall back on if the new application doesn’t work out.

Take the medical exam if required. Show up rested, hydrated, fasted if they asked you to. You want your best health numbers.

Wait for full approval. Not conditional approval. Not “we’re probably going to approve.” Full, final, unconditional approval with the policy issued and in your hands.

Step 5: Review the New Policy Carefully

You got approved. Great. Now read the actual policy document they send you.

Verify the coverage amount matches what you applied for. Check that all the riders you wanted are actually included. Make sure the premium matches what you were quoted. Confirm the policy type is what you expected.

Look at the free look period. Most policies give you 10 to 30 days to review and cancel if you change your mind. Know when that window closes.

If anything looks wrong or different from what you agreed to, contact the company immediately. Don’t assume it’s a small mistake that doesn’t matter.

Step 6: Let the New Policy Take Effect

Here’s where people mess up. They cancel their old policy the same day the new one is approved.

Don’t do that.

Wait until the new policy is actually in force. That means the first premium has been paid and accepted. The policy has an official start date that’s already passed. You’re covered.

Some insurance agents in Texas recommend waiting even longer. Like 30 days or even through the entire free look period. That way if you find any issues with the new policy, you can cancel it and still have your original coverage intact.

Step 7: Cancel Your Old Policy (Finally)

Only now, after your new coverage is active and you’re satisfied with it, do you cancel the old policy.

Contact your old insurance company in writing. Email is fine, but get written confirmation. Don’t just stop paying and assume it’ll cancel. Depending on the policy type, that could cause problems.

If you have a permanent policy with cash value, understand what happens to that value. Some policies let you take it as cash. Others might have surrender charges. Some let you use it to buy paid-up term insurance. Know your options.

Get written confirmation that the old policy is cancelled. Keep this documentation. You want proof that you properly terminated the old coverage.

Step 8: Update Your Beneficiaries and Records

You’ve got a new policy. Make sure all your information is current and correct.

Verify your beneficiaries are listed exactly as you want them. Full legal names, relationship to you, percentage of death benefit. Include contingent beneficiaries too.

Update your records at home. Your spouse or family should know where to find the new policy documents. Tell them the company name, policy number, your agent’s contact information.

Let your financial advisor, estate attorney, or anyone else involved in your financial planning know about the change. They might need to update their records or adjust other parts of your estate plan.

Common Mistakes When Switching Life Insurance Policies

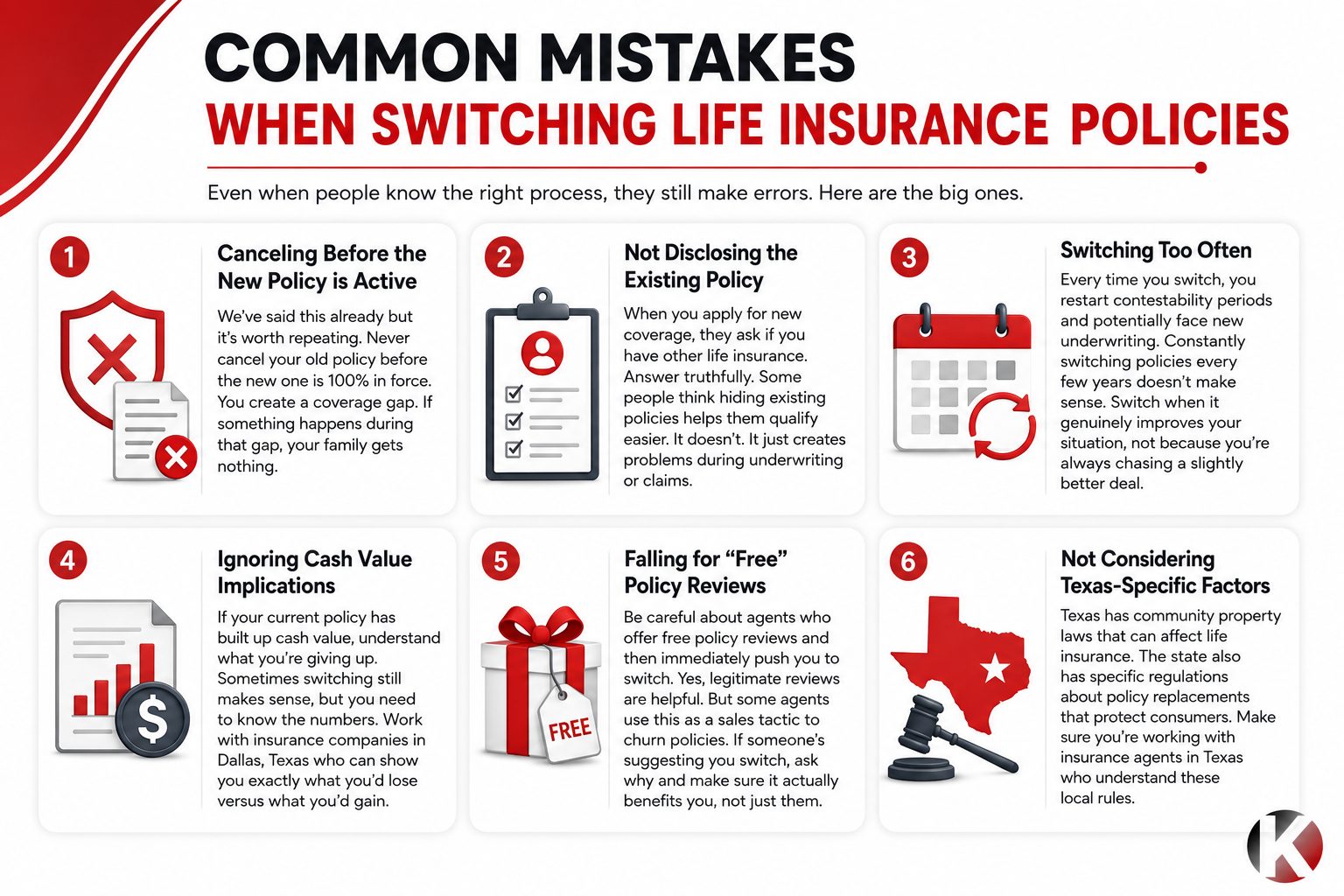

Even when people know the right process, they still make errors. Here are the big ones.

Canceling Before the New Policy is Active

We’ve said this already but it’s worth repeating. Never cancel your old policy before the new one is 100% in force. You create a coverage gap. If something happens during that gap, your family gets nothing.

Not Disclosing the Existing Policy

When you apply for new coverage, they ask if you have other life insurance. Answer truthfully. Some people think hiding existing policies helps them qualify easier. It doesn’t. It just creates problems during underwriting or claims.

Switching Too Often

Every time you switch, you restart contestability periods and potentially face new underwriting. Constantly switching policies every few years doesn’t make sense. Switch when it genuinely improves your situation, not because you’re always chasing a slightly better deal.

Ignoring Cash Value Implications

If your current policy has built up cash value, understand what you’re giving up. Sometimes switching still makes sense, but you need to know the numbers. Work with insurance companies in Dallas, Texas who can show you exactly what you’d lose versus what you’d gain.

Falling for “Free” Policy Reviews

Be careful about agents who offer free policy reviews and then immediately push you to switch. Yes, legitimate reviews are helpful. But some agents use this as a sales tactic to churn policies. If someone’s suggesting you switch, ask why and make sure it actually benefits you, not just them.

Not Considering Texas-Specific Factors

Texas has community property laws that can affect life insurance. The state also has specific regulations about policy replacements that protect consumers. Make sure you’re working with insurance agents in Texas who understand these local rules.

What About Converting Instead of Switching?

Sometimes you don’t need to switch to a completely new policy. You can convert your existing one.

Most term life policies have conversion options. This lets you convert some or all of your term coverage to permanent coverage without a medical exam. The premium will go up because permanent costs more than term. But you don’t have to go through underwriting again.

Conversion makes sense when your health has declined since you bought the term policy. Or when you realize you want lifetime coverage but you might not qualify for a new policy at good rates anymore.

There’s usually a deadline for conversion. Maybe you can convert any time during the term, or maybe only within the first 10 years, or before age 65. Check your current policy to see what your conversion options are.

If conversion is available and makes sense for your situation, it’s often safer than switching to a completely new policy with a new company.

Switching policies is just one part of building the right life insurance strategy.

Learn how to compare policies, determine the right coverage amount, and choose the best protection for your family.

Explore The Complete Guide to Life Insurance in Texas

Working With the Right Insurance Agents Texas

Switching life insurance isn’t something you should figure out on your own. There’s too many ways to mess it up.

The right insurance agencies in Texas can compare multiple carriers for you. They know which insurance companies in the town are more flexible with certain health conditions. They understand Texas regulations around policy replacements.

Good agents will actually tell you if switching doesn’t make sense. If your current policy is solid and switching would hurt you, they’ll say so. They’re not just trying to make a sale.

Look for agents who represent multiple companies, not captive agents who only sell one carrier’s products. Independent agents can show you options from several insurers and help you make a genuine comparison.

At keen coverage, we walk people through this process all the time. We’ll review your current policy, compare it to what’s available now, and give you straight answers about whether switching helps you or not.

Questions to Ask Before You Switch

Before you commit to switching, get clear answers to these questions.

Will I qualify for the new policy at the rates quoted? Don’t assume. Get a realistic assessment based on your current health and situation.

What happens to my cash value if I have it? Know the exact numbers. Understand surrender charges, loan balances, anything that affects what you’d actually get.

Am I restarting contestability periods? Yes, you are. Every new policy has a two-year contestability window. Make sure you’re comfortable with that.

What am I gaining by switching? Be specific. Better coverage amount? Lower premiums? More features? Make sure the gain is real and meaningful.

What am I giving up? Every switch involves tradeoffs. Maybe you’re giving up cash value, or your original policy had great riders, or you’re losing years of built-up policy history. Know what you’re trading away.

How long is the free look period on the new policy? You want time to review the new policy and make sure it’s what you expected.

What’s my backup plan if the new application gets denied? This is important. If you can’t qualify for the new policy, what’s Plan B? Usually that’s keeping your current policy, but make sure.

Make the Switch Safely and Smartly

Switching life insurance policies absolutely can improve your coverage and your situation. But only if you do it the right way.

The key is keeping your old policy active until your new policy is fully in force. No gaps. No risks. Not hoping it all works out.

Work with experienced insurance agents texas who can guide you through the process. Compare real options from multiple insurance companies in Dallas Texas. Get everything in writing. Read the fine print. Ask questions.

And if it turns out switching doesn’t actually help you? That’s okay too. Sometimes the best move is sticking with what you’ve got.

Frequently Asked Questions

Usually 4 to 8 weeks from start to finish. You’re applying for new coverage, which includes underwriting and possibly a medical exam. Then you need to wait for approval, get the policy in force, and only then cancel the old one. Don’t rush this. It’s better to take extra time and do it safely than to hurry and create coverage gaps.

Sometimes yes, sometimes no. Depends on what health problems you have and how severe they are. If your health got worse since your original policy, switching might not work in your favor. The new company will price you based on your current health. Work with insurance agencies Texas who can give you a realistic assessment before you apply.

Possibly, if your whole life policy has accumulated cash value. When you cancel a whole life policy, you might face surrender charges and you’ll give up any cash value above what you’ve paid in. Sometimes switching still makes sense financially, but you need to run the actual numbers. Don’t just guess.

Usually yes, unless you’re converting within your existing policy. Any new policy with a new company typically requires fresh underwriting. That often includes a medical exam, especially for larger coverage amounts. Some simplified issue or guaranteed issue policies skip the exam, but those usually cost more and have limitations.

Absolutely. Lots of people carry multiple policies. You might have term coverage through work plus a personal policy you bought yourself. Or term coverage for your mortgage plus permanent coverage for estate planning. Just make sure you can afford all the premiums and that the total coverage makes sense for your situation.

This is exactly why you never cancel the old policy before the new one is approved and active. If you made this mistake and got denied, contact your old insurance company immediately. Depending on how long it’s been, you might be able to reinstate the old policy. But it’s not guaranteed, which is why following the right order matters so much.

Get Expert Help Switching Your Life Insurance Policy

Switching life insurance policies the wrong way can leave your family unprotected. Switching the right way can save you money and give you better coverage.

At keencoverage.com, we help Texas families navigate policy switches safely. We’ll review your current coverage, show you what else is available from top insurance companies in Dallas Texas, and walk you through every step of the switching process.

No pressure. No games. Just straight answers about whether switching actually helps you or not.

Ready to explore your options? Get a policy review and comparison quote. We’ll compare your current policy against what’s available now and show you the real numbers. Then you can make an informed decision about whether switching makes sense for your family.

Contact keencoverage.com today. Work with insurance agents in Texas who put your family’s protection first, not just another commission.

Want to make sure you’re choosing the best life insurance policy for your needs?

Our life insurance guide walks you through everything from policy types and premiums to underwriting and beneficiary planning.

Start Reading The Complete Guide to Life Insurance in Texas

This article is for informational purposes only and does not constitute legal or financial advice. Coverage options and eligibility vary by carrier and individual circumstances. Please consult a licensed insurance professional like Keen Coverage for guidance specific to your situation.