You’re probably not reading this because things are going great. Maybe your renewal just came in higher than last year and nobody could explain why. Maybe a claim got complicated and you realized your policy wasn’t set up the way you thought. Or maybe you’re brand new to this and you’re trying to figure out what you actually need before you haul your first load.

Whatever brought you here, we’re glad you’re looking into this before something goes sideways. At Keen Coverage, we’ve got an entire division built around trucking, and the most common call we get isn’t from people planning ahead. It’s from truckers dealing with a denied claim, a coverage gap, or a compliance issue that could have been prevented.

We wrote this guide to change that. This is everything you need to understand about commercial truck insurance in Texas, laid out the way we’d explain it to a client sitting across from us. Not the legal version. Not the carrier’s version. Ours.

We’re an independent brokerage, which means we work for you, not the insurance company. When we shop for your coverage, we’re going to multiple carriers. When something goes wrong, we’re in your corner. That’s how we operate, and that’s the perspective this guide comes from.

Why Getting This Wrong Is So Costly in Texas

Texas isn’t a small market. This state runs on freight. I-35 through Dallas and Fort Worth is one of the busiest commercial corridors in the country. I-10 across West Texas, I-20 heading east, the Houston Ship Channel feeding product everywhere. If you’re hauling in Texas, you’re operating in a high-volume, high-scrutiny environment.

That means more accidents, more cargo claims, and more regulatory eyes on your operation. The FMCSA is not forgiving about lapses, and neither are the shippers and brokers who’ll pull your lanes the minute they see an insurance gap on your certificate.

What we see at Keen Coverage is that most trucking insurance problems aren’t about bad luck. They’re about policies that weren’t built to match the actual operation. A trucker running regional loads out of Dallas picks up a load that crosses state lines. Their intrastate-only policy doesn’t respond the way they expected. Or an owner-operator leased to a carrier assumes they’re covered driving home empty. They’re not. These aren’t fringe cases. We deal with situations like this regularly.

Commercial truck insurance in Texas isn’t just a legal checkbox. It’s what protects your truck, your cargo, your drivers, and the business you’ve built. Getting it right from the start is a lot cheaper than figuring it out after a loss.

The Coverage Types You Need to Know

Here’s the thing about trucking insurance: it’s not one policy. It’s a stack of coverages, and which ones you need depends entirely on how your operation works. Let’s walk through each one.

Primary Liability: Your Non-Negotiable Foundation

Primary liability is what covers you when your truck causes an accident. Bodily injury, property damage to other people, that’s what this handles. You can’t operate legally without it. The FMCSA sets the minimums, and those minimums vary based on what you’re hauling and whether you’re crossing state lines.

Here’s what we tell our clients at Keen Coverage: the federal minimum exists to keep you legal, not to fully protect your business. If your truck is involved in a serious accident, the exposure can go well beyond those floors, especially if you’re hauling high-value freight or operating heavy equipment. We always have a conversation about where your actual risk sits before we decide what limit makes sense.

Motor Truck Cargo Insurance: Protecting What You’re Paid to Haul

A lot of truckers assume their liability policy covers the load. It doesn’t. Liability covers damage you cause to others. Cargo insurance covers the freight you’re hauling if it’s damaged, stolen, or lost.

Lose a load without cargo coverage and you’re paying for it out of pocket, plus dealing with a shipper who probably won’t call you again. We’ve helped clients structure cargo policies around their specific freight types because not all cargo policies work the same way. High-value electronics haul differently than dry goods, and your policy should reflect that.

Physical Damage: Covering Your Equipment

Your truck is your business. If it’s sitting in a shop or totaled by the side of the road, you’re not making money. Physical damage coverage has two components: collision, which pays when your truck is in an accident, and comprehensive, which covers fire, theft, weather, vandalism, and other non-collision damage.

If you’re financing your truck, your lender’s going to require this. If you own it outright, going without it is a gamble. We’ve seen what happens when a $120,000 truck gets totaled and there’s no physical damage coverage on it. It’s not a situation anyone wants to be in.

Bobtail Insurance: When You’re Moving Without a Load

This one catches a lot of owner-operators off guard. When you’re leased to a carrier and you’re actively hauling their freight, their policy typically covers you. But the moment you drop that trailer and you’re driving home, or you’re heading out to pick up your next load, you may not be under their policy anymore.

Bobtail insurance is specifically for those stretches. It’s not expensive coverage, but the gap it fills is real. We ask every owner-operator we work with whether they understand exactly when their carrier’s coverage starts and stops. A lot of them aren’t sure. That uncertainty is what bobtail insurance fixes.

Non-Trucking Liability and Trailer Interchange

Non-trucking liability (NTL) covers you when you’re using your truck for personal use while not under dispatch. It’s different from bobtail in that bobtail is typically for commercial use outside of dispatch, while NTL is for personal use. The line between the two matters when a claim happens.

Trailer interchange is a separate coverage that applies when you’re pulling a trailer that belongs to someone else under a trailer interchange agreement. Without it, if that trailer gets damaged, you’re looking at paying for equipment you don’t even own. We make sure our clients understand which situations each of these covers.

Workers’ Compensation: Know Where Texas Stands

Texas is the only state that doesn’t mandate workers’ comp for private employers. That sounds like flexibility, but it creates real exposure. If one of your drivers gets hurt on the job and you don’t have workers’ comp, you’re dealing with that claim directly. And many freight brokers and shippers now require proof of workers’ comp before they’ll put freight on your truck.

For any trucking operation with employees, we almost always include workers’ comp in the conversation. The decision to carry it or not should be intentional, not an oversight.

How Commercial Truck Insurance in Dallas Works by Vehicle Type

We get questions all the time from truckers who assume one policy type fits every vehicle. It doesn’t work that way. The equipment you’re running shapes what coverage options are available, what underwriters are looking for, and what your premium is going to look like.

18-Wheelers and Tractor-Trailers

This is the most regulated segment of trucking, and for good reason. Tractor-trailers are heavy, they haul significant loads, and they operate across state lines. The compliance requirements are detailed, the underwriting is rigorous, and the premiums reflect the exposure.

When we work with 18-wheeler operators on commercial truck insurance in Dallas and beyond, we’re looking at driver history, CSA scores, the commodities being hauled, and the lanes being run. All of it feeds into the quote, and all of it affects which carriers will write the risk.

Hotshot Trucking

Hotshot operators are one of the groups we see most commonly underinsured. Running a pickup and flatbed doesn’t feel like big commercial trucking, so a lot of hotshots try to operate under personal auto or basic commercial auto policies. Those policies aren’t built for freight-for-hire operations, and carriers can deny claims on that basis.

Commercial trucking insurance in Texas covers hotshot operations properly. If you’re hauling for hire in Texas, even regionally, you need a commercial trucking policy. We can get that structured in a way that fits a smaller operation without overcharging you.

Dump Trucks

Dump truck work comes with elevated exposure. You’re often operating on or near construction sites, navigating roads with heavy equipment traffic, and hauling materials that can cause significant damage if something goes wrong. The environments are rougher on the equipment too.

When we quote dump truck insurance for Texas operators, we’re factoring in the type of work being done, where the trucks are operating, and what’s being hauled. Quarry and mining work rates differently than residential construction.

Flatbed Trucks

Flatbed carriers deal with load securement issues more than almost any other truck type. A load that shifts or falls creates liability that goes beyond what a basic cargo policy might cover. The cargo coverage terms on a flatbed policy need to be looked at carefully.

We work with flatbed operators to make sure the cargo policy is built around the kinds of loads they’re actually running, whether that’s construction materials, machinery, or oversized freight with special permitting requirements.

Tow Trucks

Tow truck insurance is its own category, and general commercial truck policies typically won’t cover it correctly. On-hook coverage, which protects the vehicle you’re towing, is specific to tow operations and needs to be part of the policy. Roadside exposure is also different from over-the-road trucking.

We work with tow operators in the Dallas area regularly and understand how these policies need to be structured. It’s not complicated once you know what you’re looking for, but a generic commercial truck policy is usually not the right fit.

Box Trucks

Box trucks are everywhere in commercial truck insurance in Dallas TX, used for everything from last-mile delivery to moving companies to catering operations. The coverage that’s right depends a lot on what the truck is doing and who’s driving it.

If drivers are employees, workers’ comp becomes part of the picture. If you’re using contractors, the coverage structure changes. We get into those details because they affect how a claim would actually be handled.

Owner-Operator vs. Fleet: How Your Business Structure Shapes Your Coverage

If You’re an Owner-Operator

Whether you’re leased to a carrier or running under your own authority, your insurance situation is unique to your setup. We spend a lot of time with owner-operators at Keen Coverage because the coverage gaps in this segment are real and they’re not always obvious.

If you’re leased, the first thing we want to understand is exactly what the carrier’s policy covers and when it applies. That determines what you need to carry yourself. If you’re on your own authority, you’re building the full coverage stack from scratch, and the combination of primary liability, cargo, physical damage, and specialty coverage has to actually fit how you operate.

If You’re Running a Fleet

Fleet programs make sense once you’re managing multiple units. A single fleet policy simplifies your administration and can get you better pricing when your safety record is solid. But fleet programs also come with more underwriting scrutiny. Every driver on your roster affects the quote.

We help fleet operators at Keen Coverage think through driver qualification programs, how to present their fleet to underwriters, and how to structure coverage so it actually fits the scale of the operation.

Large Fleets and Captive Insurance

If your annual trucking insurance spend has grown to a significant level, there’s a conversation worth having about captive insurance. A captive is a company-owned insurance entity that lets you retain more of your own risk and build equity over time instead of paying premiums to a traditional carrier year after year.

It’s not the right answer for every operation, and it takes time to set up properly. But for fleets that have gotten large enough, it can fundamentally change how you manage insurance costs. We’ve covered this in more depth in our piece on why captive insurance is a long-term financial strategy. We have those conversations at Keen Coverage with clients who’ve reached that scale. If it might apply to you, let’s talk.

FMCSA Compliance and Texas Requirements: What You’re Actually Responsible For

Compliance is the part of trucking insurance that nobody finds exciting until something goes wrong. We’re going to keep this practical.

What the FMCSA Requires

If you’re operating as a for-hire motor carrier in interstate commerce, the FMCSA requires you to have insurance on file with them before you can operate. The mechanism for that is Form MCS-90, an endorsement that your insurer files directly with the FMCSA confirming your coverage is in place.

Minimum liability limits under FMCSA rules depend on what you’re hauling. General freight, hazmat, and passengers each have different thresholds. BMC-91 and BMC-91X are related filings for property brokers and freight forwarders. If you’re brokering loads in addition to hauling them, the filings you need look different.

Texas Intrastate Rules

Texas manages intrastate operations through the TxDMV. If you’re only operating within Texas, you’re dealing with state requirements rather than federal ones, though the two can overlap depending on your commodity and equipment type.

Here’s where truckers get caught: if you haul within Texas 95% of the time and cross a state line occasionally, you need interstate coverage. Intrastate-only policies are written for operations that genuinely never cross. We make sure commercial truck insurance in Texas reflects how an operation actually works, not just the most favorable interpretation.

Coverage Lapses and What They Cost You

We’ve seen what a coverage lapse does to a trucking operation. The FMCSA can pull your authority. Shippers check certificates before they release loads, and a gap on your certificate of insurance means they’ll put that freight on a different truck. If an accident happens during a lapse, there’s no policy to respond to it.

Part of what we do at Keen Coverage is track renewals and make sure our clients don’t fall into those gaps. It sounds simple, but for a busy owner-operator or a fleet manager juggling a lot of moving parts, renewals get missed. We make sure they don’t.

Why Your Premium Is What It Is

Premium is usually the first question and often the most frustrating one. Here’s how we explain the factors to our clients.

Driver History and CSA Scores

Your drivers’ histories are probably the biggest factor in your rate. Accidents, violations, and claims follow a driver’s record. CSA scores from the FMCSA tell underwriters how your operation has performed on inspections and roadside stops. Poor scores mean higher rates, sometimes significantly higher.

For fleets, the whole roster matters. One driver with a rough history can affect what the entire fleet pays. We help fleet operators understand this when they’re making hiring decisions, because the insurance impact is real.

What You’re Hauling

Dry van general freight rates differ from fuel, chemicals, refrigerated products, or high-value electronics. The commodity affects how underwriters see the risk. It also affects which carriers are willing to write the policy at all. Some carriers won’t touch certain commodity types regardless of the operator’s history.

When we’re shopping commercial truck insurance in Texas for a client, the cargo type is one of the first things we clarify because it shapes the entire market we’re going to.

How Far You’re Running

Local and regional operations typically rate lower than long-haul. More miles on the road is more exposure time, and underwriters price accordingly. Texas-only operations generally rate differently than lanes that go into the northeast or out to the west coast.

Your Equipment

Older trucks cost more to insure, both because mechanical failure risk is higher and because older equipment lacks the safety technology that newer trucks have. Dashcams, collision avoidance, electronic logging all factor into how underwriters look at a fleet. Investing in equipment upgrades can have a real effect on what you pay.

How Long You’ve Been Operating

New trucking authorities are genuinely harder to place. There’s no loss history, no track record, no evidence of how the operation manages risk. We work with new operators and we know how to present a new authority to carriers in a way that gets them competitive options. But it’s honest work, not a shortcut. The track record gets built over time, and the rates follow.

Mistakes We See Texas Truckers Make

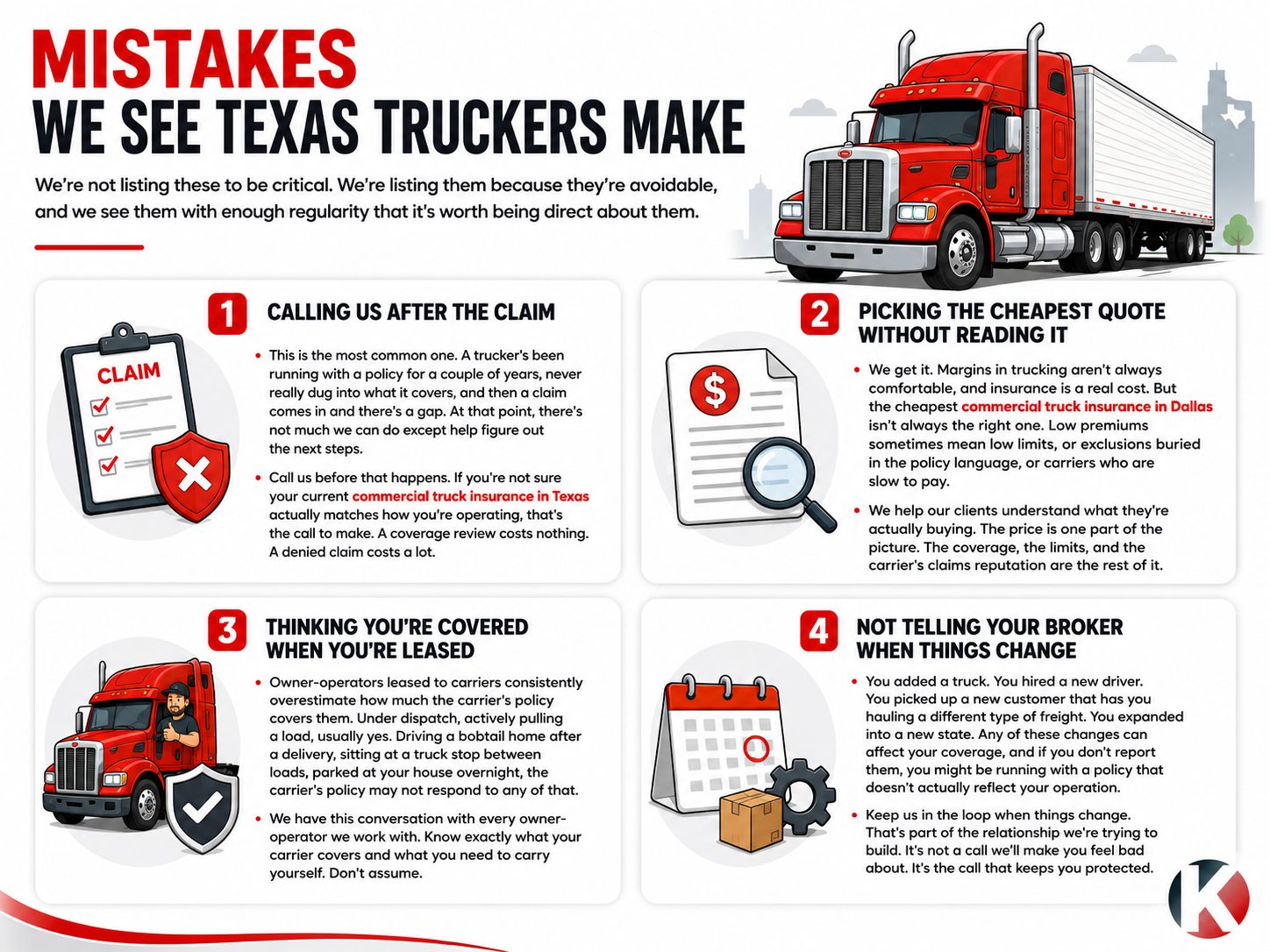

We’re not listing these to be critical. We’re listing them because they’re avoidable, and we see them with enough regularity that it’s worth being direct about them.

Mistake 1: Calling Us After the Claim

This is the most common one. A trucker’s been running with a policy for a couple of years, never really dug into what it covers, and then a claim comes in and there’s a gap. At that point, there’s not much we can do except help figure out the next steps.

Call us before that happens. If you’re not sure your current commercial truck insurance in Texas actually matches how you’re operating, that’s the call to make. A coverage review costs nothing. A denied claim costs a lot.

Mistake 2: Picking the Cheapest Quote Without Reading It

We get it. Margins in trucking aren’t always comfortable, and insurance is a real cost. But the cheapest commercial truck insurance in Dallas isn’t always the right one. Low premiums sometimes mean low limits, or exclusions buried in the policy language, or carriers who are slow to pay. We’ve written about the hidden costs businesses overlook when selecting insurance that apply directly here.

We help our clients understand what they’re actually buying. The price is one part of the picture. The coverage, the limits, and the carrier’s claims reputation are the rest of it.

Mistake 3: Thinking You’re Covered When You’re Leased

Owner-operators leased to carriers consistently overestimate how much the carrier’s policy covers them. Under dispatch, actively pulling a load, usually yes. Driving a bobtail home after a delivery, sitting at a truck stop between loads, parked at your house overnight, the carrier’s policy may not respond to any of that.

We have this conversation with every owner-operator we work with. Know exactly what your carrier covers and what you need to carry yourself. Don’t assume.

Mistake 4: Not Telling Your Broker When Things Change

You added a truck. You hired a new driver. You picked up a new customer that has you hauling a different type of freight. You expanded into a new state. Any of these changes can affect your coverage, and if you don’t report them, you might be running with a policy that doesn’t actually reflect your operation.

Keep us in the loop when things change. That’s part of the relationship we’re trying to build. It’s not a call we’ll make you feel bad about. It’s the call that keeps you protected.

What Working With Keen Coverage Actually Looks Like

We want to be specific here because ‘we represent you, not the carrier’ is something a lot of agencies say. Here’s what that actually means in practice.

Understanding the role of an insurance broker in risk mitigation makes the difference between a policy that’s built for your operation and one that just looks good on paper. When you come to us for commercial truck insurance in Dallas TX, we’re not going to hand you a one-page application and come back with a single quote. We’re going to ask about your operation. How many trucks, what types, what commodities, what routes, how long you’ve been running, what your drivers’ histories look like, whether you’ve had claims, what you’re paying now and whether you know why. That conversation matters because it’s what lets us build a picture of your risk before we go to the market.

Then we go to multiple carriers. Not one. Multiple. We have access to commercial truck insurance carriers across the country, and for commercial truck insurance in Texas specifically, we’ve built relationships with carriers who understand this market. We bring back options with real explanations of what each one covers and where the differences are.

After you’re placed, we handle the compliance side. FMCSA filings, certificate issuance, renewal management. We’re not going to send you a renewal notice in the mail two weeks before expiration and call that service. Proof of insurance documentation is something shippers and brokers check before every load, and we make sure your certificates are always current and accurate.

And when a claim happens, we’re involved. That doesn’t mean we control what the carrier does, but it means you’ve got someone who understands your policy explaining what’s going on, following up, and making sure the claim process moves forward.

That’s what working with us looks like. If it sounds like what you’re looking for, reach out.

How to Evaluate Your Coverage: A Practical Checklist

If you want to review your current coverage or shop for new coverage, here’s the order we’d recommend working through it.

- Write down exactly how your operation works. Truck types, commodity types, routes, whether you’re leased or on your own authority, how many drivers you have. Don’t rely on how you described your operation to the last broker. Describe it accurately now.

- Check your compliance requirements. Are you operating interstate or intrastate? What does the FMCSA require for your cargo type? What does Texas require? Make sure your current policy is actually meeting those requirements.

- Pull out your current policy and look at the limits. Not just the coverage types, the limits. A cargo policy that’s half of your typical load value isn’t actually protecting you.

- Read the exclusions section. This is the part most people skip. It’s also the part that determines whether your claim gets paid. Ask your broker to walk through it with you.

- Get at least one second opinion. If you’ve been with the same carrier or agent for years and you’ve never shopped it, you probably don’t know if you’re getting a competitive rate. We’d be glad to give you a comparison.

- When something in your operation changes, tell your broker. New truck, new driver, new freight type, new territory. Changes that aren’t reported are the ones that create gaps.

- Set a calendar reminder 90 days before renewal. That’s enough lead time to properly shop your coverage instead of scrambling at the last minute.

Signs It’s Time to Call Keen Coverage

You don’t need to wait for a problem to give us a call. But here are some situations where we’d especially encourage you to reach out.

- You’re getting your first trucking authority and you need to get coverage in place before you haul.

- Your renewal came in significantly higher than last year and you weren’t given a clear reason why.

- You’ve had a claim and you’re not satisfied with how it was handled.

- You recently added trucks or drivers and you haven’t updated your policy.

- You’re unsure whether your carrier’s policy covers you during the gaps between loads.

- Your fleet has grown to the point where a fleet program or an alternative risk structure might make more sense.

- You want someone to just look at your current coverage and tell you honestly whether it’s the right fit.

We don’t push people into coverage they don’t need. If your current policy is solid, we’ll tell you that. If there are gaps, we’ll show you exactly what they are and give you options for addressing them.

Before You Go

Commercial truck insurance in Texas isn’t optional, and it’s not something to set up once and forget about. Your operation changes. Rates change. Your risk changes. The coverage that made sense two years ago might have gaps today that you’re not aware of.

At Keen Coverage, we built our trucking division because we saw what happened to operators who didn’t have the right coverage when they needed it. We wanted to offer something different. An independent brokerage that actually takes the time to understand your operation, shops your risk across multiple carriers, handles your compliance, and is available when claims happen.

If you’re running commercial truck insurance in Dallas or anywhere in Texas, we’d be glad to talk through your situation. Visit us at keencoverage.com or call 833-245-2157. No pressure, no sales pitch. Just a conversation about whether your coverage actually fits.

Frequently Asked Questions

Commercial trucking insurance isn’t a single policy. It’s a combination of coverages built around your operation. At minimum, it includes primary liability, which covers damage you cause to others. Beyond that, cargo insurance covers the freight you’re hauling, physical damage covers your truck, and specialty coverages like bobtail, non-trucking liability, and trailer interchange fill the gaps that standard policies don’t. What you need depends on how you operate. That’s why we start every client conversation with questions about the actual operation before we talk about coverage.

The legal minimums exist, but they’re a floor, not a recommendation. The FMCSA sets minimums for interstate carriers based on cargo type. Texas sets requirements for intrastate carriers. Most operators should be carrying limits that reflect their actual exposure, not just what keeps them technically legal. A shipper’s load value, your equipment value, the type of routes you run, all of those feed into what the right limits look like for your operation. We work through that with every client.

We start by understanding your operation before we touch a quote. Once we know what you’re running, what you’re hauling, and what your history looks like, we go to multiple carriers and come back with real options. We explain what each policy actually covers, where the differences are, and what we’d recommend and why. After placement, we handle filings, certificates, and renewals. And when you have a claim, we’re involved in making sure it moves forward properly. That’s the whole picture.

Yes, if you’re hauling freight for hire. The specific requirements depend on whether you’re operating interstate or intrastate, what you’re hauling, and what type of authority you’re operating under. No-coverage or wrong-coverage situations aren’t just compliance problems. They’re financial exposure problems. If an accident happens and your policy doesn’t respond because it wasn’t set up correctly, that’s on you personally.

Driver history is usually the biggest factor. CSA scores, accidents, violations, all of it shows up in the underwriting. Beyond that, the commodity type, operating radius, equipment age, and how long the operation has been running all affect the rate. New authorities pay more than established ones. Fleets with clean safety records pay less than those with claims history. Working with a broker who can shop your risk across multiple carriers helps make sure you’re getting the most competitive number for your specific profile.

Bobtail insurance covers you when you’re driving your truck without a trailer, specifically during times when you’re not under dispatch with your carrier. A lot of owner-operators who are leased to carriers assume they’re covered all the time. They’re not. The carrier’s policy responds when you’re actively pulling their loads. When you’re in between, the coverage typically doesn’t apply. Bobtail fills that window. It’s not expensive coverage, and the gap it fills is real.

It creates problems fast. The FMCSA can revoke your operating authority. Shippers and brokers check certificates before releasing freight, and a lapse means they’ll move that load to someone else. If an accident happens during the gap, you have no insurance to respond to claims. The financial and legal exposure can be significant. Staying current on coverage is something we actively help our clients manage, including tracking renewals so the gap never happens in the first place.

We can review what happened and help you understand why the denial occurred and what your options are. Honestly, though, the better version of this conversation happens before the claim, not after. If you’re not sure your current commercial truck insurance in Texas is structured correctly, that’s the time to call us. We can review your coverage, identify gaps, and get things corrected before a loss forces the issue.