Here’s the thing about buying life insurance in Texas. It should be straightforward. You’re protecting your family’s future, plain and simple.

But walk into most insurance offices and you’ll walk out more confused than when you started. We see it constantly. A couple from Dallas sits down thinking they’ll get a simple answer about coverage. Two hours later, they’re drowning in jargon, second-guessing everything, and wondering if they just signed up for way more than they need.

Or take the Houston dad who skipped the medical exam because he was too busy. Sure, he got coverage faster. He’s also paying double what he should be. Then there’s the San Antonio business owner who went with the first quote she got because it seemed reasonable. Turns out three other companies would’ve given her better coverage for less.

These aren’t rare situations. This is what happens every single day across Texas.

The good part? None of these mistakes have to happen to you.

We’ve worked with thousands of Texas families at keencoverage.com, and we’ve spotted patterns. The same errors keep coming up. People mean well. They just don’t know what they don’t know. And honestly, why would they? Most folks buy life insurance once, maybe twice in their entire life.

So let’s break down the 10 biggest mistakes we see Texans make when buying life insurance. More importantly, let’s talk about how you sidestep every single one of them.

Mistake #1: Shopping Without Comparing Multiple Insurance Companies in Dallas, Texas (and Beyond)

This happens all the time. Someone talks to one agent, gets one quote, signs the paperwork. Done and done, right?

Not quite.

Life insurance rates are all over the map, even for identical coverage. We’re talking about the same death benefit, same term length, same everything. One company might charge a 35-year-old non-smoker in Austin one amount, while another company charges something completely different. For the exact same policy.

And here’s where it gets interesting. Most people only look at the big national names they’ve seen on TV. Makes sense. You recognize the brand, you trust it. But Texas has dozens of solid regional carriers that locals have never heard of. Insurance companies in Dallas, Texas, for instance, sometimes run special programs for DFW residents that the national players don’t even know exist.

You wouldn’t buy a car from the first dealership you visit. The same logic applies here.

Here’s what works better: Pull quotes from at least three different companies. Better yet, five. Work with insurance agencies in Texas that represent multiple carriers, not just one. That way you’re comparing real options, not just taking what’s in front of you. At keencoverage.com, we pull quotes from all our top-rated carriers at once. You see everything, then decide.

Mistake #2: Buying Too Much Coverage (or Not Nearly Enough)

We see both ends of this spectrum every week.

There’s the person who buys a massive policy because bigger must be better, right? Then six months later they’re struggling to keep up with the payments. Eventually they let the policy lapse. Now they’ve got nothing.

Then there’s the flip side. Someone grabs whatever coverage their employer offers and calls it good. Usually that’s nowhere near enough to actually protect their family. Their kids still need to go to college. The mortgage still needs to get paid. One income doesn’t cut it anymore.

Neither situation is ideal.

Here’s the real question: what happens to your family if you’re not around tomorrow? Do you have a mortgage that needs covering? Kids who’ll need help paying for school? A spouse who’d have to jump back into the workforce after years of being home? Maybe you’ve got business debts that wouldn’t just disappear?

All of this matters when you’re figuring out how much coverage you actually need.

Better approach: There’s this thing called the DIME method. Stands for Debt, Income, Mortgage, Education. It’s a decent starting point for calculating what you need. Most experts say aim for about 10 to 12 times your annual income. But that’s really just a ballpark. Insurance agents in Texas worth their salt will sit down and run the numbers based on your actual situation, not some cookie-cutter formula.

Mistake #3: Not Understanding the Difference Between Term and Permanent Life Insurance

Alright, this one trips people up constantly. And honestly, it’s probably the most expensive mistake on this whole list.

So here’s the deal with term life insurance. It covers you for a set period. Could be 10 years, 20 years, 30 years. You pick the term when you buy it. It’s straightforward, and it doesn’t cost an arm and a leg.

Permanent life insurance, on the other hand, is what it sounds like. It lasts your whole life. Whole life, universal life, those are both types of permanent coverage. These policies build cash value over time, which sounds great. They also cost way more than term insurance.

The problem happens when people end up with the wrong type. Like when someone buys a whole life policy thinking they need it, when really a term policy would’ve done exactly what they wanted. Or the opposite happens too. Someone grabs term insurance when they actually need permanent coverage for estate planning stuff.

The premium difference between these two types is huge. Like, really huge. For a lot of Texas families, term insurance makes total sense. Cover the years when the kids are growing up and you’re paying off the house. But if you’re worried about estate taxes or you want to leave a guaranteed inheritance, permanent coverage might be worth it.

What you should do: Be real about what you’re trying to accomplish. Need coverage while you’re raising kids and paying the mortgage? Term insurance is probably your answer. Want to make sure your final expenses are covered no matter when you go, or planning to leave money to your kids? Look at permanent options. Just don’t let someone talk you into the expensive option without explaining exactly why you need it.

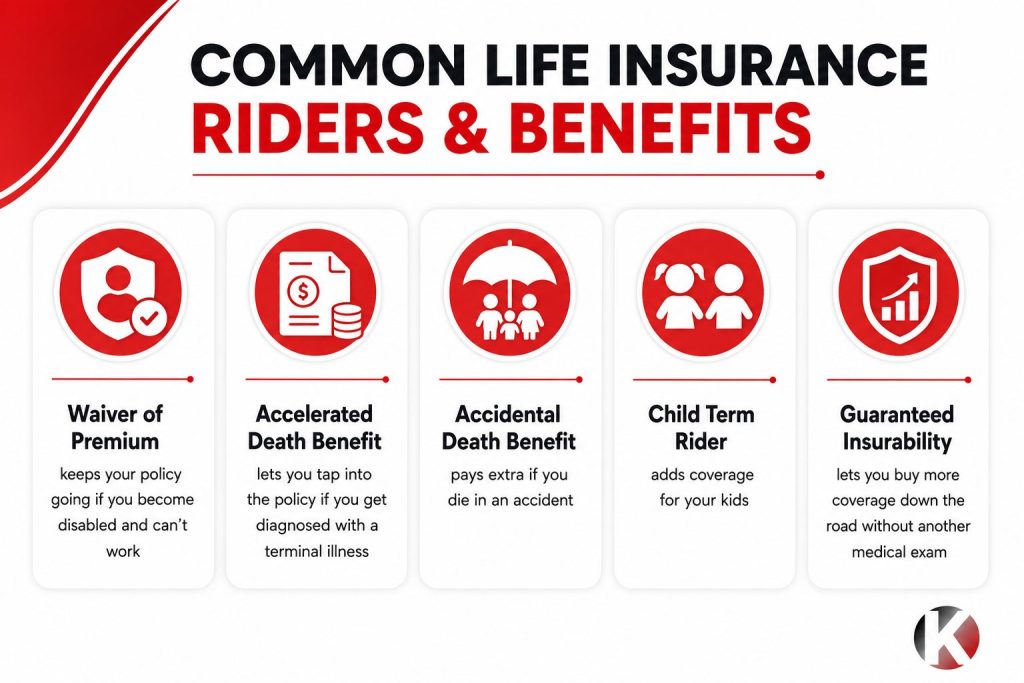

Mistake #4: Skipping Important Riders That Could Save Your Family

Policy riders. Most people have never even heard the term, let alone know what they do.

Think of riders as add-ons to your main policy. They extend your coverage in ways that might actually matter to your family. And a lot of Texans don’t even know these exist.

Here are some common ones:

- Waiver of premium keeps your policy going if you become disabled and can’t work

- Accelerated death benefit lets you tap into the policy if you get diagnosed with a terminal illness

- Accidental death benefit pays extra if you die in an accident

- Child term rider adds coverage for your kids

- Guaranteed insurability lets you buy more coverage down the road without another medical exam

Most of these riders add barely anything to your monthly payment. But when you need them, they can be worth thousands.

Smarter move: Sit down with your agent and go through what’s available. At minimum, look into waiver of premium and accelerated death benefit. They’re cheap insurance on top of your insurance, if that makes sense. Most families end up glad they added them.

Confused About Life Insurance?

Our complete guide to Life Insurance in Texas simplifies everything from term life to whole life coverage.

Mistake #5: Being Less Than Honest on Your Application

Okay, this is where things get serious.

Some people think they’re being clever. They downplay health issues. Conveniently forget to mention certain medications. Say they quit smoking when they really didn’t. Figure what the insurance company doesn’t know won’t hurt them.

Bad idea. A really bad idea.

Know what happens when your family files a claim? The insurance company digs into everything. And we mean everything. They pull medical records, check prescription databases, look at driving records. If they find out you weren’t straight with them on the application, they can slash the death benefit or deny the whole claim.

Your family ends up with way less than they expected. Or nothing at all.

Texas insurance law doesn’t mess around with this stuff. Full disclosure is required. That speeding ticket from two years ago? Yeah, mention it. Blood pressure medication? That too. Your weekend skydiving hobby? Absolutely include it.

Insurance companies have access to more information than you think. They will find out. Count on it.

What you need to do: Answer every single question honestly. All of them. Will some health issues bump up your rate? Probably. But at least you’ll actually be covered when it matters. Working with experienced insurance agencies in Texas helps because they know the market. They know which carriers go easier on certain conditions. Someone with diabetes might get a better deal with one company. High blood pressure? Different companies might be your best bet.

Mistake #6: Naming the Wrong Beneficiary (or No Beneficiary at All)

Beneficiary mistakes are a nightmare for families who are already grieving. We’ve seen it too many times.

Common screwups include naming minor kids directly as beneficiaries. Sounds logical, except kids under 18 can’t legally receive life insurance money. Or someone gets divorced, remarries, but never updates their beneficiary. Guess who the money goes to? The ex-spouse. Awkward doesn’t begin to cover it.

Then there’s the people who forget to name backup beneficiaries. Your primary beneficiary dies before you do, and suddenly nobody knows where the money should go. Or folks write “my children” without actually naming them. Which children? All of them? Just biological? Stepkids too?

These little details create huge legal messes. We’ve watched Texas families get stuck in probate court for months trying to sort out beneficiary issues. All because of vague or outdated paperwork.

Do this instead: Name specific people using their full legal names. If you want money to go to minor children, set up a trust. Always name contingent beneficiaries as backup options. And here’s the big one: review your beneficiaries every couple years. Definitely check them after major life stuff like getting married, divorced, having kids, or when someone passes away.

Mistake #7: Treating Life Insurance as “Set It and Forget It”

Your life doesn’t stay the same. Why should your coverage?

That policy you picked up at 28 when you were single and renting an apartment? Fast forward ten years. Now you’re 38 with two kids and a mortgage. That old policy probably isn’t cutting it anymore.

Or look at it from the other direction. Maybe you bought a big policy when your kids were little and money was tight. Now they’re 30 with their own careers and families. You might not need as much coverage as you thought.

Life changes. Coverage should change with it.

Better plan: Pull out your policy every couple years and take a fresh look. Definitely review it after big life events. Got married? Had a baby? Bought a house? Changed jobs? Got divorced? All of those are good reasons to reassess what you need. Insurance agents in Texas can help you figure out if you should adjust up or down. A lot of term policies even let you convert to permanent coverage if your situation changes and you decide you need it.

Mistake #8: Choosing a Policy Based Only on Price

Cheapest doesn’t always mean the best deal. Sometimes it just means cheap.

Sure, premiums matter. Nobody wants to overpay. But there’s other stuff you need to think about. Like is this insurance company actually going to be around in 20 years? Do they have a track record of paying claims, or do they fight families every step of the way? Can you actually get someone on the phone when you have questions?

A company that charges slightly less but has a reputation for denying claims isn’t doing you any favors. They’re setting your family up for a fight when they’re already dealing with losing you.

Texas has solid consumer protection laws, but you still want a carrier with good ratings. Look for an A- or better from AM Best. That tells you the company is financially stable and reliable.

Smarter approach: Compare the whole package, not just the monthly payment. Check out company ratings. Read what actual customers say. Ask about their claims process. Insurance companies in Dallas, Texas, and across the state vary a ton in quality. At keencoverage.com, we only work with carriers that have proven they pay claims fairly and quickly. No point in having coverage if your family has to fight for it later.

Mistake #9: Not Working with Local Insurance Agents Who Understand Texas

National call centers and online calculators are fine for some things. Life insurance? Not so much.

Texas has its own insurance regulations. Its own tax rules. Its own market conditions. An agent in another state might miss details that matter here. For example, Texas is a community property state. That affects how life insurance money gets treated in estate planning. A local agent knows this stuff. Some generic online form doesn’t have a clue.

Plus, when you’ve got questions or you need to file a claim, talking to a real person you can actually meet with makes a world of difference. Insurance agencies in Texas can work with your financial planner, your estate attorney, your tax person, making sure everything fits together the way it should.

What works better: Partner up with insurance agents in Texas who actually understand how things work here. Look for agents who take time to learn about your whole financial picture, not just someone trying to hit their sales numbers. The right agent becomes a resource for your family long-term, not just someone who sells you a policy and disappears.

Mistake #10: Waiting Too Long to Buy Coverage

This one costs people more than any other mistake on this list.

Every year you wait, life insurance gets pricier. Every birthday means higher payments. Every new health issue that pops up means higher payments or possibly getting turned down altogether.

A healthy 30-year-old will pay way less than if they wait until they’re 40 for the same coverage. Wait until you’re 50 and dealing with some health stuff? Your options get limited fast, and what’s available gets expensive in a hurry.

And here’s the thing nobody wants to think about. None of us knows what tomorrow brings. That surprise diagnosis. That car wreck. That heart attack nobody saw coming. Life doesn’t wait for a convenient time. You put this off and something happens, you’ve missed your chance to protect your family. That’s it. Game over.

Here’s what you do: Buy life insurance when you’re young and healthy. Even if you think you don’t need much right now, locking in low rates while you can makes financial sense. At keencoverage.com, we help Texans get covered fast. Streamlined applications, quick approvals, no runaround.

Make Smart Decisions About Your Family’s Financial Future

Life insurance really isn’t that complicated when someone explains it in plain English.

Avoid these 10 mistakes and you’ll end up with coverage that actually protects your family without wrecking your budget. Simple as that.

Best time to buy life insurance? Ten years ago. Second best time? Right now, today.

Don’t wing it on something this important. Don’t just take the first quote that lands in front of you. And definitely don’t leave your family’s financial security up to chance or good luck.

Frequently Asked Questions

It depends on a bunch of factors. Your age, your health, how much coverage you’re buying, what type of policy you want. Younger, healthier folks generally pay less than older applicants or people dealing with health issues. Your best bet is getting personalized quotes from multiple insurance companies in Dallas, Texas, and around the state. That’s how you find the best rate for your specific situation.

Even single people without kids often benefit from having coverage. Think about it. Do you have student loans? A mortgage? Aging parents who might need help? Business partners who’d be stuck with your debts? Want to leave something to charity? A lot of single Texans grab smaller policies to cover final expenses and debts. It keeps parents or siblings from inheriting a financial mess.

Yeah, most people with health conditions can still get coverage. Your rate might be higher, but conditions like diabetes, high blood pressure, or past cancer don’t automatically disqualify you. Working with experienced insurance agents in Texas helps a lot here. They know which carriers are more flexible with specific health issues and can shop your case around to multiple companies.

Term life covers you for a specific time period, like 20 years. Costs less but doesn’t build any cash value. Whole life lasts your entire life, builds cash value you can borrow against, but costs way more. Most Texas families go with term because it’s affordable and straightforward. You get protection during your working years without breaking the bank.

Check their AM Best rating. Look for A- or higher. Read customer reviews online. Verify they’re licensed in Texas through the Texas Department of Insurance website. Ask about their history of paying claims. Reputable insurance agencies in Texas only work with financially solid, well-rated carriers. They’re not going to risk their reputation on sketchy companies.

Employer coverage is a decent start but usually not enough for most families. Plus you lose it if you change jobs or get laid off. Most financial experts say get your own policy on top of whatever work offers. That way you’ve got continuous protection and enough coverage no matter what happens with your job.

Ready to Protect Your Texas Family the Right Way?

Look, you don’t have to figure this out alone.

At keen coverage, we connect Texas families with the right coverage without the hassle or confusion. Our team works with top-rated insurance companies across Texas to find you options that actually fit your budget and what you need to protect.

We’ll help you sidestep these expensive mistakes and feel confident about the decisions you’re making for your family’s future.

Get your quote today. Compare rates from multiple carriers in just a few minutes. Talk with knowledgeable insurance agents who actually understand Texas and how things work here. Get the protection your family deserves without the runaround.

Continue Reading: The Complete Guide to Life Insurance in Texas

Discover everything Texans need to know about finding the right life insurance policy.