Someone walks into our office (or calls, or emails) and says something like this: “I’ve got life insurance, so I’m covered if I need nursing home care, right?”

And we have to be the ones to break it to them. No. That’s not how it works.

At Keen Coverage, we’ve had this conversation hundreds of times with people across Texas. The confusion between long-term care insurance and life insurance is massive. And it’s understandable, honestly. Both involve insurance. Both are about protecting your future. Both cost money you’d rather spend on literally anything else.

But here’s the thing. They protect you from completely different financial disasters. Mixing them up could leave you or your family in a really bad spot down the road.

So let’s clear this up once and for all.

What Life Insurance Actually Does

Life insurance is pretty straightforward. You die, your beneficiaries get money. That’s it.

The whole point is income replacement and debt coverage. If you’re the breadwinner and you kick the bucket, your spouse and kids don’t lose the house. Your business partner can buy out your share. Your final expenses get paid without draining the family savings.

Term life gives you coverage for a set period. 10 years, 20 years, 30 years, whatever. You pay premiums, and if you die during that time, boom, your beneficiaries get the death benefit. If you don’t die? The policy expires and you get nothing back. Which is actually good because it means you’re still alive.

Permanent life (whole life, universal life) stays in force your entire life and builds cash value. Costs more, but you’re guaranteed a payout eventually because, well, everyone dies eventually.

Our team works with clients throughout Texas who need various types of life insurance. Someone in Dallas might need $2 million in term coverage for business obligations. Someone in Houston might want a permanent policy for estate planning. Different situations, different solutions.

But here’s what life insurance doesn’t do. It doesn’t pay for anything while you’re alive. Not your medical bills. Not your nursing home stay. Not the home health aide you need three times a week.

Life insurance is for after you’re gone. Period.

What Long-Term Care Insurance Actually Covers

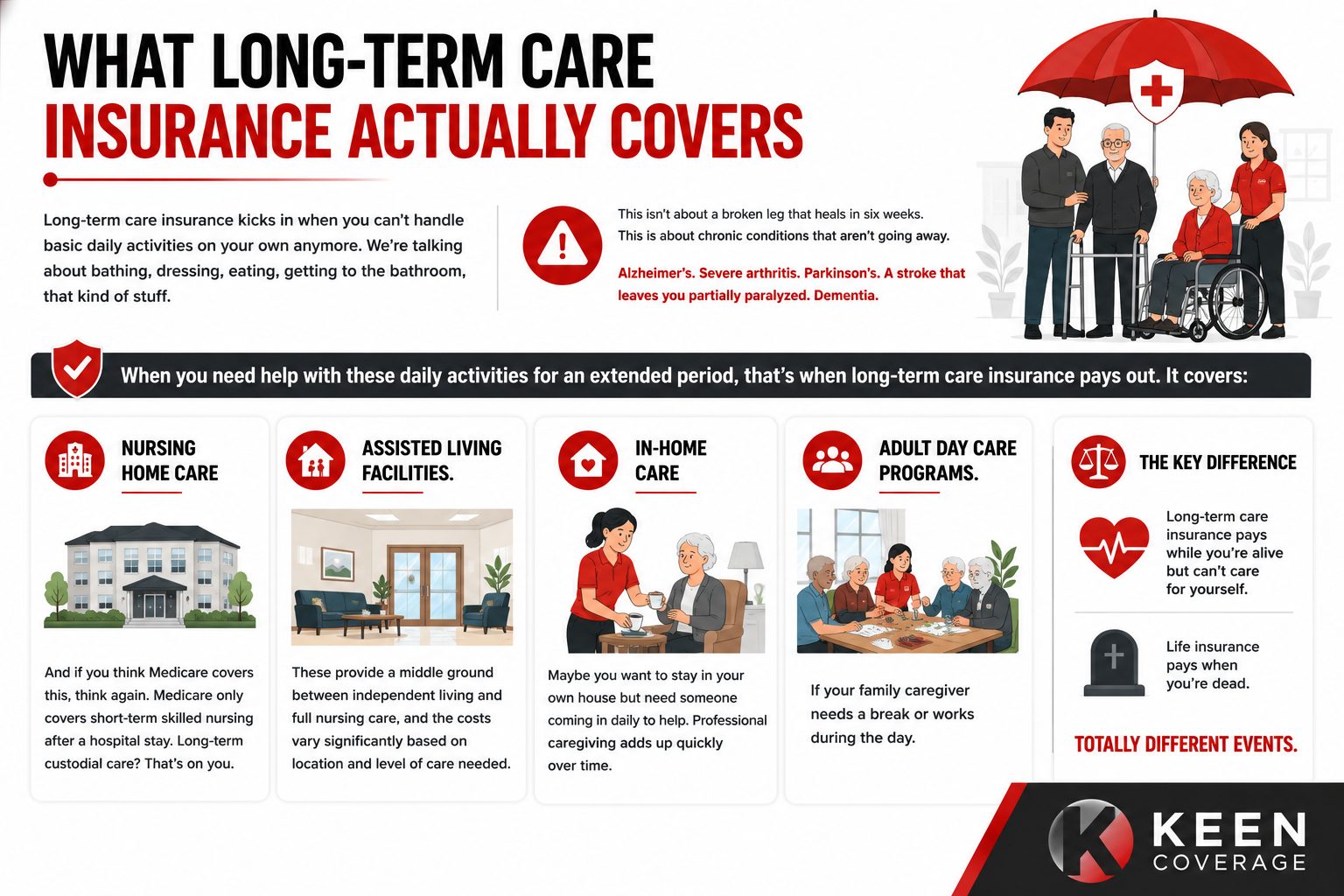

Long-term care insurance kicks in when you can’t handle basic daily activities on your own anymore. We’re talking about bathing, dressing, eating, getting to the bathroom, that kind of stuff.

This isn’t about a broken leg that heals in six weeks. This is about chronic conditions that aren’t going away. Alzheimer’s. Severe arthritis. Parkinson’s. A stroke that leaves you partially paralyzed. Dementia.

When you need help with these daily activities for an extended period, that’s when long-term care insurance pays out. It covers:

Nursing home care. And if you think Medicare covers this, think again. Medicare only covers short-term skilled nursing after a hospital stay. Long-term custodial care? That’s on you.

Assisted living facilities. These provide a middle ground between independent living and full nursing care, and the costs vary significantly based on location and level of care needed.

In-home care. Maybe you want to stay in your own house but need someone coming in daily to help. Professional caregiving adds up quickly over time.

Adult day care programs. If your family caregiver needs a break or works during the day.

The key difference insurance agents in Texas explain to clients all the time: long-term care insurance pays while you’re alive but can’t care for yourself. Life insurance pays when you’re dead. Totally different events.

Confused about which policy fits your financial goals? Explore our complete guide to life insurance in Texas to compare coverage options, costs, and benefits before making a decision.

The Reality Nobody Expects

Here’s where people’s eyes get really wide during our conversations at Keen Coverage.

Life insurance, especially term life, is generally more affordable than most people think. You can get substantial coverage without breaking the bank.

Long-term care insurance? That’s a different story entirely. The premiums are significantly higher, and if you wait until you’re older to buy it, they increase substantially.

Why the huge difference? Because you’re way more likely to need long-term care than you are to die during your term life policy period. Insurance companies price based on risk, and the risk of needing long-term care is high.

About 70% of people over 65 will need some form of long-term care. That’s not a small number. And the average stay in a nursing home is 2-3 years, though it can be much longer.

We’ve worked with families in Dallas who’ve watched their retirement savings disappear into nursing home bills. Years of care costs can wipe out a lifetime of saving pretty quickly.

When You’re Young: Which One Matters More?

If you’re in your 30s or 40s with a family and a mortgage, life insurance wins. Hands down. Not even close.

Your biggest financial risk right now is dying unexpectedly and leaving your family without income. Your kids need to eat. Your mortgage needs to get paid. Your spouse needs to keep living their life without financial disaster.

Long-term care? That’s a future problem. Could you need it? Sure. But it’s not the immediate risk.

Our team at Keen Coverage typically recommends young families focus on getting solid life insurance coverage first. Make sure you’ve got enough term life to cover your obligations. Then, if there’s room in the budget, maybe look at disability insurance next (because you’re more likely to become disabled than die young, honestly).

Long-term care insurance can wait until your 50s for most people.

When You’re Older: The LTC Question Gets Real

Once you hit your 50s, especially as you approach 60, the long-term care conversation needs to happen.

Your kids are probably grown. Maybe the house is paid off or close to it. You’ve built up retirement savings. Your need for massive life insurance coverage has decreased.

But your risk of needing long-term care is climbing. And this is where we see a lot of people in Texas making a critical mistake. They keep pumping money into life insurance they don’t really need anymore while completely ignoring the LTC risk that’s actually more likely to hit them.

We worked with a couple in Austin last year. Both in their early 60s, healthy, good retirement savings. They had substantial life insurance coverage but zero long-term care protection.

We asked them: “If one of you needs nursing home care, where’s that money going to come from every month?”

They looked at each other. They hadn’t thought about it. They assumed Medicare would cover it (it won’t, not long-term). They assumed their life insurance would somehow help (it won’t, unless they die).

After running the numbers, they reduced their life insurance coverage and used the savings to fund long-term care policies. Made way more sense for their actual risk profile.

Long-term care insurance and life insurance serve different purposes, but both play a role in financial planning. Discover everything you need to know in our complete guide to life insurance in Texas.

The Hybrid Option Nobody Talks About

Here’s something interesting that insurance companies in Dallas, Texas, and across the country have started offering. Hybrid policies that combine life insurance and long-term care coverage.

These policies give you a death benefit like regular life insurance. But if you need long-term care, you can access part of that death benefit early to pay for it.

So you’re not stuck with the “use it or lose it” aspect of traditional long-term care insurance. If you never need care, your beneficiaries still get the life insurance payout. If you do need care, the policy helps pay for it.

Sounds perfect, right? Well, sort of.

The catch is they’re expensive. And the long-term care portion usually isn’t as comprehensive as a standalone LTC policy. But for some people, especially those who hate the idea of “wasting” money on traditional long-term care insurance they might never use, hybrids make sense.

We help clients evaluate these at Keen Coverage. Sometimes they’re the right fit. Sometimes they’re not. Depends on your goals, budget, and how you feel about insurance in general.

What Happens If You Have Neither

Let’s talk about the worst-case scenario. You need long-term care, you don’t have LTC insurance, and you’re still alive so life insurance isn’t helping.

Your options:

Pay out of pocket. Hope your retirement savings can handle the monthly care expenses indefinitely. For many people, this drains everything they saved their whole life.

Lean on family. Your kids become your caregivers. This is hard on everyone. They’re trying to work, raise their own kids, and now they’re helping you to the bathroom and managing your medications. It strains relationships.

Medicaid. Once you’ve spent down almost all your assets, Medicaid will cover nursing home care. But you get what you get in terms of facility choice. And you’ve lost your life savings to qualify.

We’ve seen all of these scenarios play out with families across Texas. It’s brutal. And the thing is, it’s often preventable with the right planning.

Common Mistakes People Make

Thinking Life Insurance Covers Long-Term Care

Biggest one. Your life insurance policy doesn’t pay anything until you die. If you’re in a nursing home for five years and then die, the life insurance eventually pays your beneficiaries. But it did nothing to cover those five years of care costs.

Assuming Medicare Covers Everything

Medicare covers short-term skilled nursing care after a hospitalization. It does NOT cover long-term custodial care. We see this misconception constantly. People retire thinking they’re covered, and then reality hits.

Waiting Too Long to Get LTC Insurance

The older you get, the more it costs. Also, the harder it is to qualify. Develop diabetes, have a heart issue, anything that makes you higher risk, and premiums skyrocket or you get declined entirely.

Our agents in Texas usually suggest looking at LTC insurance in your mid-50s if you can afford it. Not too early where you’re paying premiums for decades, not too late where it’s prohibitively expensive.

Getting Too Much or Too Little Coverage

Some people go overboard and buy more coverage than they’ll ever need. Others cheap out and get a policy that won’t actually cover their costs when the time comes.

You need to think about: how much does care cost in your area of Texas? How much can you afford to pay out of pocket? What coverage amount fills that gap?

Working with experienced insurance agencies in Texas who understand the local cost of care makes this calculation way easier.

How Your Family Situation Matters

Single with no kids? Your calculus is different from someone with a spouse and three children.

If you’re single, you probably need less life insurance. Who are you protecting? But long-term care becomes more critical because you don’t have a built-in caregiver. If something happens, you’re relying on paid help or facilities.

Married with a younger spouse? Life insurance protects them if you die. LTC insurance protects both of you from the financial drain of care costs. If you need care, it doesn’t wipe out the retirement savings your spouse needs to live on.

Have aging parents you’re already helping support? You’re getting a preview of what’s coming. This should be a wake-up call to get your own LTC coverage sorted before you’re in the same boat.

The Texas Perspective on Coverage

Different states have different costs for care and different insurance regulations. In Texas, long-term care costs vary significantly by region.

Dallas and Houston metro areas? More expensive. Smaller cities? More affordable. Rural areas? Fewer options but generally lower costs.

Insurance companies in Dallas, Texas, and throughout the state offer policies that reflect local costs. When our team helps you evaluate options, we’re looking at what care actually costs where you live or where you plan to retire.

Also, Texas doesn’t have state income tax, which means more of your money is available for insurance premiums. That’s actually an advantage when you’re trying to fit both life insurance and LTC coverage into your budget.

Making the Decision

Here’s how we walk clients through this at Keen Coverage:

Start with your age and life stage. Young family? Life insurance first. Approaching retirement? LTC needs more attention.

Look at your budget. What can you actually afford in premiums? Maybe you can’t do everything at once. Prioritize based on your biggest risk.

Consider your family health history. If Alzheimer’s or other conditions requiring long-term care run in your family, LTC insurance moves up the priority list.

Think about your retirement savings. If you’ve got millions saved, you might be able to self-insure for long-term care. If your nest egg is more modest, insurance becomes critical.

Talk to experienced insurance agents in Texas who understand both products. Our team at Keen Coverage specializes in helping people figure out the right mix of coverage. We’re not just selling you something. We’re analyzing your actual situation and recommending what makes sense.

The Bottom Line

Life insurance and long-term care insurance solve different problems.

Life insurance replaces your income and pays off debts when you die. It’s for your family’s financial security after you’re gone.

Long-term care insurance pays for assistance with daily living when you can’t take care of yourself anymore. It’s for protecting your savings and maintaining dignity during a difficult time.

Most people need both at some point in their lives. The question isn’t usually “which one?” It’s “when do I need each one, and how much?”

Get the Right Coverage for Your Situation

At Keen Coverage, we work with individuals and families across Texas to build comprehensive insurance strategies that actually make sense for their lives.

Whether you’re in Dallas, Houston, Austin, San Antonio, or anywhere else in the state, our insurance agents in Texas can help you understand your options for both life insurance and long-term care coverage.

We work with top-rated insurance companies in Dallas, Texas, and throughout the country to find you the best policies at competitive rates. We’re not tied to one carrier, which means we can shop your needs across multiple companies.

Get your insurance consultation at today. Let’s talk about your specific situation and figure out what coverage makes sense now and what you should plan for down the road.

Our insurance agents in Texas have helped thousands of people protect their families and their financial futures. Let us do the same for you.

Stop guessing about coverage. Get real answers from insurance agencies in Texas that know the market inside and out.

Questions People Ask Us All the Time

Not while you’re alive. Life insurance only pays out when you die. Some policies have accelerated death benefit riders that let you access part of the death benefit if you’re terminally ill, but that’s different from regular long-term care needs. If you need nursing home care and you’re not dying imminently, your life insurance sits there doing nothing to help with those bills.

This is the gamble everyone struggles with. About 70% of people over 65 need some form of long-term care, so there’s a pretty good chance you’ll use it. But yeah, 30% won’t. Our take at Keen Coverage: it’s insurance. You hope you never need it, just like you hope your house doesn’t burn down. But if you do need it, not having it can financially devastate your family. The peace of mind is worth something.

Most experts (including our team) recommend looking at it in your mid to late 50s. Earlier than that and you’re paying premiums for a long time before you might need it. Later than that and it gets really expensive or you might not qualify health-wise. The sweet spot is usually 55-60 years old.

No. This is the biggest misconception we encounter. Medicare covers short-term skilled nursing care after a hospital stay, up to 100 days under specific conditions. But long-term custodial care in a nursing home or assisted living? Medicare doesn’t pay for that. Once your savings are gone, Medicaid might cover nursing home care, but that means you’ve already lost everything.

Absolutely, and most people should have both at different life stages. When you’re young with dependents, life insurance is critical. As you age and your kids are grown, long-term care insurance becomes more important. You can also get hybrid policies that combine both, though they might not provide optimal coverage for either purpose compared to standalone policies.